FameEX Crypto Market Trend | July 8, 2026

2026-07-08 07:33:47

ECB hikes, U.S.-Iran peace deal reopening the Strait of Hormuz while Bitcoin fell with tech stocks; U.S. unemployment hit 4.2% in June, lowest since June 2025.

I. Core Market Overview

1. BTC Spot Performance

Price Range: 57,773 USD - 65,573.5 USD

Weekly Volatility: 13.5%

Key Driving Factors:

Primary Factors: The European Central Bank’s interest rate hikes. The United States and Iran reached a peace agreement, leading to the reopening of the Strait of Hormuz.

Secondary Factor: During the same period, Bitcoin plunged in tandem with U.S. technology stocks. The U.S. unemployment rate declined to 4.2% in June this year, marking its lowest level since June 2025.

2. Central Bank Policy Updates

Policy Impact Assessment:

Federal Reserve: Maintains a hawkish stance, signaling one additional rate hike this year, though a move at the end-July meeting appears unlikely.

European Central Bank: Remains focused on the rate hike path and inflation outlook, with another rate hike later this year currently appearing more likely than not.

3. Other Key Updates

Key Takeaways from the Fed’s June FOMC Statement and Chair Warsh’s Press Conference

FOMC Statement:

1) Interest Rate Decision: The Fed left the federal funds rate unchanged at 3.50%-3.75%, marking the fourth consecutive meeting with no change. All voting members unanimously approved the decision.

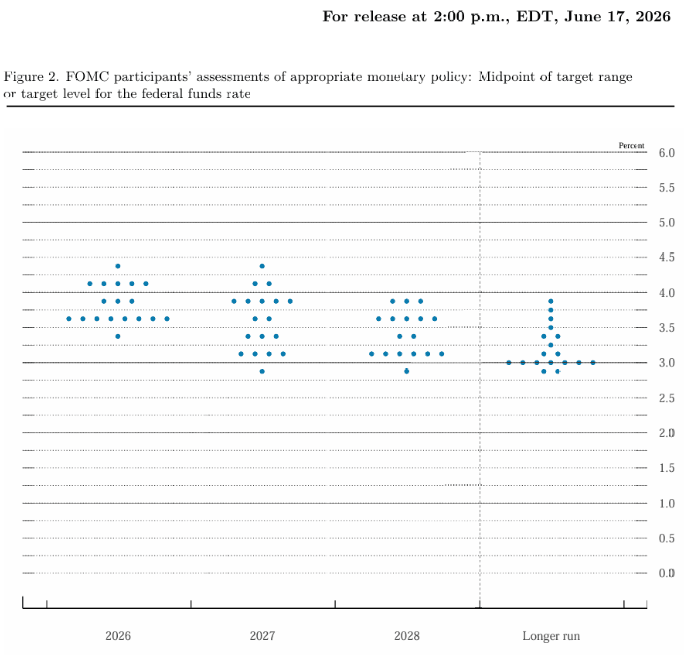

2) Rate Path: Chair Warsh did not submit a dot plot. Around half of Fed officials are considering one additional rate hike this year. The median federal funds rate projections for the next three years were revised higher, while the longer-run rate projection remained unchanged.

3) Inflation: Inflation remains above the Committee’s 2% target, and the FOMC remains committed to restoring price stability. The Fed significantly raised its forecasts for both headline PCE inflation and core PCE inflation this year.

4) Economic Outlook: Despite elevated uncertainty stemming from the Middle East conflict, economic activity continues to expand at a solid pace. The Fed slightly lowered its GDP growth forecast for this year.

5) Labor Market: Employment growth continues to keep pace with labor force growth, and the unemployment rate has changed little. The Fed slightly lowered its unemployment rate forecast for this year.

6) Communication Changes: The statement discontinued the practice of publishing individual voting records, adopted significantly more concise language, and removed wording that had implied the possibility of further rate cuts.

Chair Warsh’s Press Conference

1) Statement Overhaul: Warsh said the new policy statement is shorter and simpler, focusing on facts rather than repeating legacy language. He added that the Fed has abandoned forward guidance.

2) No Dot Plot: Warsh did not release a dot plot, saying that “the dot plot is drawn in pencil and can be erased.” He added that submitting his own dot plot would not improve policymaking.

3) New Working Groups: The Fed has established working groups across five areas of monetary policy. They will begin work in the coming weeks and are expected to complete their reviews by year-end.

4) Inflation Assessment: Warsh reaffirmed that 2% inflation remains the Fed’s long-standing objective and said there is no reason to reconsider that target before it is achieved. He noted that inflation has missed the target for five consecutive years, and the Fed must now correct that.

5) Economic Data: Warsh said some incoming economic data may simply be “echoes of the past.” He expressed openness to new analytical approaches, private-sector data, and improvements to official statistics. He added that financial market prices are among the most important sources of information for central bankers, noting that private-sector data are typically real-time and require fewer revisions than government data.

6) Labor Market: The Committee believes the labor market remains stable, with employment data continuing to improve. Warsh said the Fed does not need to choose between maximum employment and price stability.

7) Communication Review: The Fed plans to conduct a comprehensive review of its communications framework by year-end, including press conferences, the dot plot, and meeting arrangements. While he described press conferences as an effective communication tool, he emphasized that they should be reserved for conveying important information.

8) External Relations: Warsh said he has met with U.S. Treasury Secretary Bessent three times, and has also met with the Inspector General regarding the renovation of the Federal Reserve headquarters. He declined to say whether he has spoken with President Trump since taking office.

Latest Federal Reserve Dot Plot (Source: Jin10 Data)

On June 23, Grayscale Head of Research Zach Pandl said that Bitcoin could rally if the Fed pauses its rate hike cycle. Since the Iran war began in late February, U.S. equities have gained 9%, while Bitcoin has fallen 1% and gold has declined 20%. Although heavy AI-related spending has supported the stock market, Bitcoin and gold have underperformed, partly because investors expect the Fed to raise interest rates to combat inflation. Grayscale does not share this view, with its base case remaining that the Fed will pause further rate hikes. If that proves correct, Bitcoin could catch up with equities.

Pandl noted that since the outbreak of the Iran war, one-year Fed rate expectations have risen by around 60 basis points, and roughly half of Fed officials believe a rate hike in 2026 could be appropriate. Meanwhile, the ECB has already raised interest rates. As non-yielding monetary assets, both Bitcoin and gold compete with fiat currencies. Higher real interest rates increase the opportunity cost of holding these assets, weighing on demand. Pandl added that Bitcoin serves a dual role in investment portfolios. On one hand, it is a scarce digital commodity that functions as a long-term store of value. On the other, it is a public blockchain asset that provides exposure to the long-term growth of the crypto industry. As such, Bitcoin’s role in a portfolio is similar to, but not identical with, that of gold and growth stocks. If the likelihood of further Fed rate hikes declines, in line with Grayscale's base case, Bitcoin could outperform and catch up with equities.

II. Market Health Index Analysis (Source: CoinMarketCap)

Source: https://coinmarketcap.com/charts/

Conclusion:

The total cryptocurrency market capitalization is rising, while higher trading volume suggests fresh capital is gradually entering the market.

The Altcoin Season Index is in the 25-54 range, indicating capital is rotating from Bitcoin into mid- and small-cap tokens.

Net ETF inflows, combined with the Crypto Fear & Greed Index remaining in the Fear zone, suggest market confidence is beginning to strengthen.

III. Derivatives Monitor (Source: CoinAnk)

1. Funding Rate

30-Day Avg Funding Rate of Bitcoin Across the Top Six CEXs: 0.4452% (Positive)

30-Day Avg Funding Rate of ETH Across the Top Six CEXs: -0.0158% (Negative)

Source: https://coinank.com/fundingRate/current

Interpretation:

Positive funding rates indicate that long positions are dominating the market, reinforcing bullish expectations.

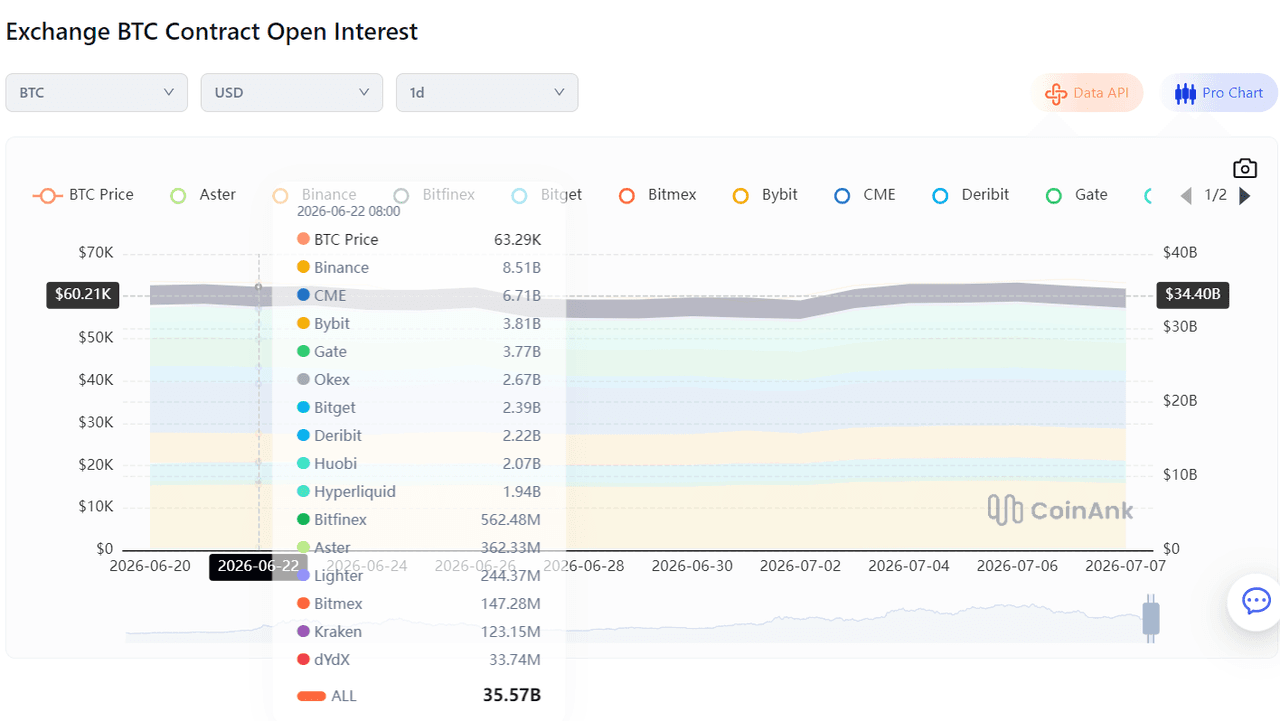

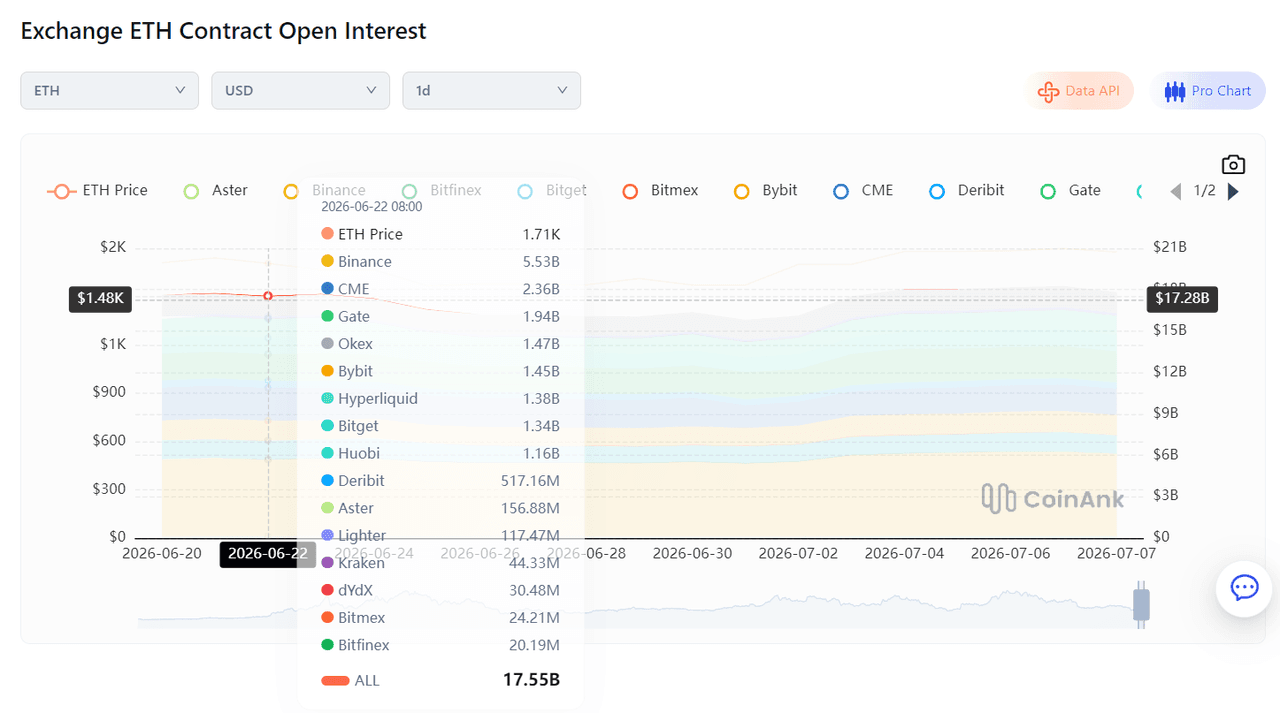

2. Open Interest Changes

Source: https://coinank.com/indexdata/oivol/exOiHist

IV. Global Economic and Crypto Sector Developments

1. Global Macroeconomy

- June 12: ECB raises interest rates by 25 basis points, marking its first rate hike in nearly three years → Outcome: Met market expectations.

- June 15: The United States and Iran reach a peace agreement, leading to the reopening of the Strait of Hormuz → Impact: Gold and cryptocurrencies rally in tandem.

- June 17: Federal Reserve interest rate decision: Upper bound 3.75% (Expected: 3.75%; Previous: 3.75%) → Outcome: Met market expectations.

1) June 22: The AI investment boom expanded upstream, with several leading U.S. semiconductor equipment companies more than doubling in value this year.

2) June 23: U.S. weekly ADP employment change for the week ending June 6 came in at 30,750, compared with 25,500 previously, weighing on gold, silver, and cryptocurrencies.

3) June 25: IMF Chief Economist Gita Gopinath said that the Fed’s gradual move away from strong forward guidance in monetary policy is "entirely appropriate."

4) June 26: Iran launched another round of missile and drone attacks against neighboring countries, including Bahrain and Kuwait.

5) June 27: U.S. Central Command said the United States launched strikes against Iran in response to attacks on commercial vessels.

6) June 29: Russian President Vladimir Putin said Russia proposed that both Russia and Ukraine halt strikes against targets deep inside each other’s territories.

7) June 30: The Bank for International Settlements (BIS) warned that market euphoria signals are emerging rapidly, and the AI spending boom could end in a prolonged "investment recession."

8) July 1: Iran prepared to sell oil to all countries except Israel.

9) July 3: The U.S. unemployment rate fell to 4.2% in June, the lowest level since June 2025, beating market expectations of 4.3%.

10) July 4: U.S. equity funds recorded $17.2 billion in net outflows for the week ending July 1, marking the first weekly outflow in three months.

11) July 5: Bank of England Monetary Policy Committee member Mann said short- and long-term inflation expectations remain elevated and that the bank is prepared to raise rates if price pressures persist.

12) July 6: Bank of England Governor Bailey said the central bank seeks to achieve its inflation target without harming economic output.

2. Industry Update

1) June 22: Japan’s nationwide corporate pension fund plans to allocate 1% of its portfolio to cryptocurrencies.

2) June 22: A crypto trading scam emerged in Russia involving the “Moscow Exchange crypto trading” scheme, with phishing websites stealing funds and user data.

3) June 23: Chainlink partnered with 47 banks in South Korea and Europe to accelerate cross-border international fund transfers.

4) June 24: BlackRock said Bitcoin can be viewed as a complementary diversification asset, recommending a modest allocation of 1%-2%.

5) June 25: The crypto market came under pressure as a sell-off in technology stocks intensified, with Bitcoin briefly falling to its lowest level since October 2024.

6) June 25: Data showed that U.S. Bitcoin ETFs recorded $6.4 billion in net outflows over the past 30 days, marking the largest monthly outflow on record.

7) June 28: Galaxy CEO said Strategy’s stock and preferred securities have become key indicators for assessing Bitcoin market risk.

8) June 29: Grayscale said Bitcoin’s bear market could evolve along two potential paths, while maintaining a long-term positive outlook on crypto assets.

9) June 29: American Express hired a Vice President of Stablecoin and Blockchain Strategy to advance stablecoin payments and tokenization initiatives.

10) June 30: The crypto industry became the largest corporate political donor in the U.S., contributing $189 million toward the 2026 midterm elections.

11) June 30: Data showed that around 84% of altcoins on Binance were trading below their 200-day moving averages, with weakness persisting for nearly eight months.

12) July 1: Coinbase’s Strategy Head said that more than 40 countries have committed to purchasing Bitcoin in some form.

13) July 2: Total top-up volume for crypto payment cards surpassed $10 billion for the first time, with stablecoins driving adoption growth.

14) July 3: Trump said he was unaware of up to $1.43 billion in crypto-related income in 2025. Trump conducted 22,000 stock trades in 2025, compared with only 13 trades during Biden’s four-year presidency.

3. Regulatory Policy Update

- Region: The European Union will implement new anti-money laundering rules on July 1, 2027, imposing a comprehensive ban on privacy coins and anonymous accounts. → [Regulatory Guidelines Issued]

1) June 22: The U.S. Independent Community Bankers of America (ICBA) called for a review of Kraken’s limited-purpose banking charter, putting pressure on the prospects of crypto firms gaining direct access to Fed payment channels.

2) June 23: The EU’s cross-border financial control mechanisms raised concerns, with the Philippines’ crypto regulatory framework facing questions over sovereignty.

3) June 24: It was reported that the U.S. Congress would hold a hearing on the CLARITY Act on July 17.

4) June 25: Trump declined to sign a bill banning a U.S. central bank digital currency (CBDC), while pushing forward election-related legislation.

5) June 26: U.S. Senate Democrats called for a hearing into a $500 million UAE investment in Trump’s crypto project, alleging potential policy conflicts of interest.

6) June 27: According to the Hong Kong Securities and Futures Commission’s annual report, the total market capitalization of virtual asset ETFs in Hong Kong has increased 90% since launch, while trading volume on licensed platforms rose 125% year-on-year.

7) June 28: Dubai’s Virtual Assets Regulatory Authority approved its 50th licensed crypto firm. Singapore has approved 37 firms, while Hong Kong has approved 13.

8) June 29: South Korea’s revised listing rules will take effect, with some KOSDAQ-listed crypto DAT companies facing delisting risks.

9) June 30: The EU has issued 244 MiCA crypto licenses, with Germany and France accounting for more than one-third of the total.

10) June 30: The UK Financial Conduct Authority (FCA) released its final crypto regulatory framework, with mandatory licensing requirements scheduled to take effect in October 2027.

11) July 1: Brazilian authorities, cooperating with U.S. sanctions efforts, froze approximately $2 billion in assets, including cryptocurrency holdings.

12) July 1: U.S. CFTC Chairman said Illinois’ proposed crypto “sin tax” legislation could threaten Chicago’s status as a global financial hub.

13) July 2: The Reserve Bank of India reiterated support for a “containment-oriented prohibition approach” toward crypto assets, recommending that banks should not hold or trade cryptocurrencies.

14) July 2: Brazil’s central bank placed crypto VASPs under regulatory requirements equivalent to securities brokers.

15) July 3: SEC Chairman said the agency is advancing the modernization of rules and regulations to facilitate the migration of markets onto blockchain infrastructure.

16) July 3: Chinese police disclosed forensic procedures for tracking and freezing cryptocurrencies in the journal Criminal Technology.

17) July 4: Taiwan passed the Virtual Asset Service Act, formally establishing a crypto regulatory framework.

18) July 5: Myanmar’s AI-driven cyber fraud operations were exposed, with Starlink serving as key infrastructure and crypto payments, OpenAI models, and Google models incorporated into the toolkit.

19) July 5: Vietnamese police reported progress in the ONUS cryptocurrency fraud investigation, seizing more than 350 kilograms of gold and silver and freezing over 300 bank accounts.

20) July 6: South Korea’s Supreme Court sought public opinions on civil enforcement rules for virtual assets.

21) July 6: The original target for signing the U.S. CLARITY Act into law on July 4 has been missed, and the window for passage before the midterm elections is rapidly narrowing.

V. Market Outlook

July 8 - August 31: A long-term trading strategy remains in place:

BTC spot: Place sell orders at $135,900, $122,500, $109,050, and $82,150. Set bottom-fishing buy orders at $49,600, $35,450, and $21,300.

ETH spot: Place sell orders at $4,885, $3,485, and $2,200, with bottom-fishing buy orders at $1,240 and $1,085.

On July 3, market analyst IT Tech, citing CryptoQuant data, said that the cumulative spot market buy-sell volume imbalance for altcoins excluding Bitcoin and Ethereum has fallen further to a five-year low, indicating continued selling pressure. Since reaching a short-term peak in early 2025, the altcoin spot market has remained in a net selling state for more than 15 months, with almost no significant rebound or meaningful easing of selling pressure. The market has yet to establish a clear bottom.

VI. Risk Alert

1. Macro Risks:

Further Federal Reserve rate hikes;

A continued sharp decline in U.S. technology stocks;

Renewed conflict between the U.S., Israel, and Iran.

2. Industry Risks:

A major crypto exchange collapse or failure.

Trading Advice:

Keep spot positions within ≤65% of total capital, and set dynamic take-profit and stop-loss levels to avoid blindly chasing rallies or selling into weakness with high leverage.

Disclaimer: The data in this report are sourced from publicly available information. FameEX makes no representations on the accuracy or suitability of any official statements made by the exchange regarding the data in this area or any related financial advice.