2026 RWA Tokenization Trends and the Rise of TradFi

2026-05-20 12:10:50

As global crypto regulation enters a more mature phase in 2026, blockchain is no longer viewed as an alternative experimental tool. It is becoming an operating system for the global financial system. In this transition, the tokenization of real-world assets, or RWAs, has emerged as one of the defining trends. This evolution is not just about changing the wrapper around an asset. It is a structural overhaul of the way securities are processed, the way settlement works, and the way capital moves. From early experiments by crypto-native platforms to the collective entry of Wall Street institutions, tokenization is breaking the geographic and time-zone barriers that have long defined traditional finance. Through programmable token wrappers, assets now gain a new level of liquidity and transparency. A new era of finance, shaped by the interaction between on-chain and off-chain systems, has already begun.

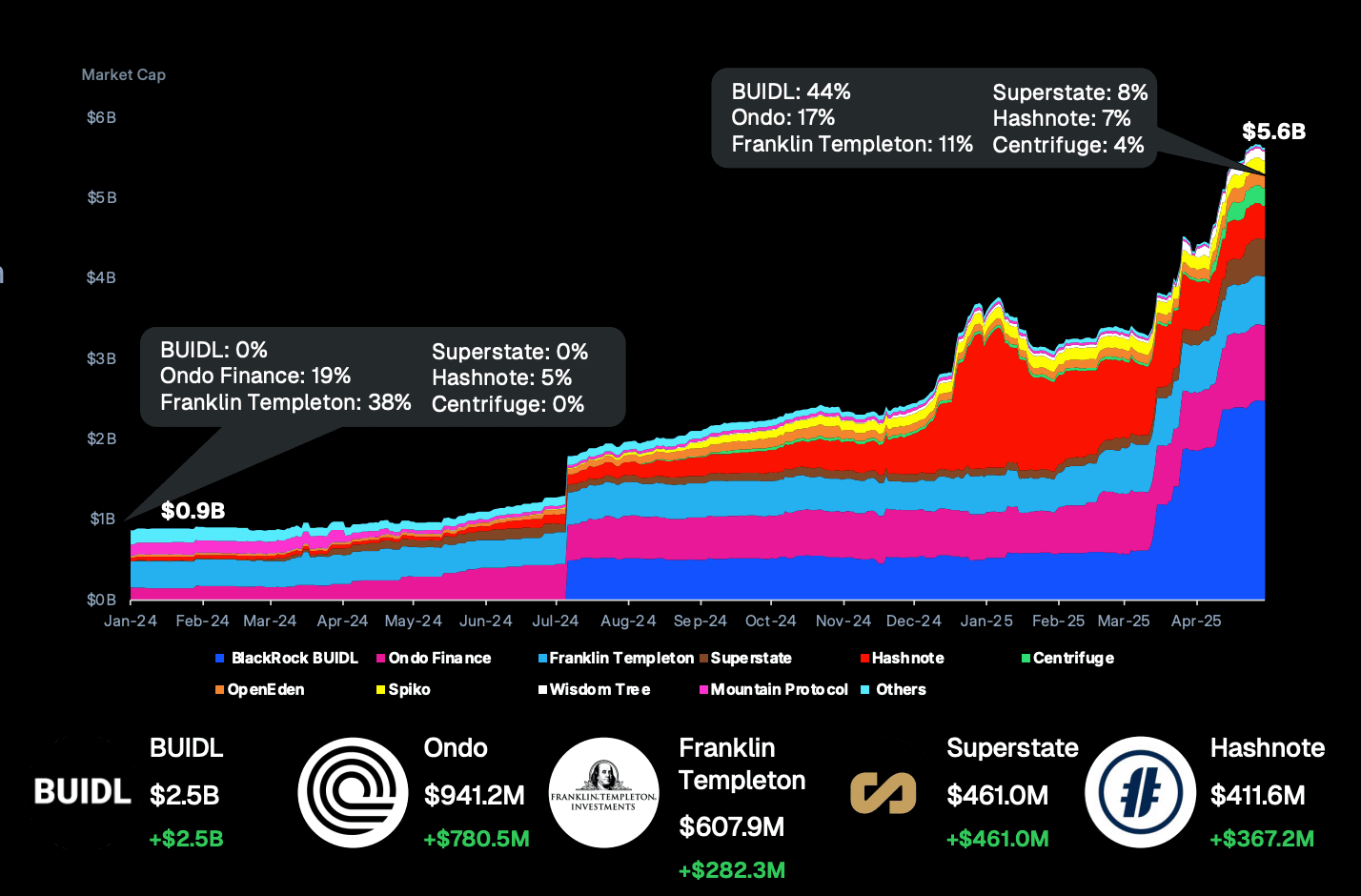

Market cap of tokenized treasuries in 2025. Source: https://assets.coingecko.com/reports/2025/CoinGecko-2025-RWA-Report.pdf

From Data to Conviction: The Exponential Rise of the RWA Market and the Shift in Narrative

According to authoritative research released in early 2026, the tokenized RWA market is approaching a breakout stage of explosive growth. Data shows that the total on-chain value of RWAs has surged from USD 5 billion in 2023 to more than USD 25 billion today. This expansion is not simply a matter of larger numbers. It reflects a much deeper shift in trust toward blockchain as a source of truth. The current market structure shows that private credit, government Treasury products, and tokenized real estate account for the majority of on-chain value. This reveals a clear investor preference in a volatile macro environment. Market participants are increasingly drawn to on-chain assets backed by underlying real assets and capable of delivering stable yield.

- Market size forecasts: Research institutions such as Keyrock and Securitize suggest that by 2030, the distributed RWA market (assets that can move freely on-chain) could grow to USD 400 billion, while the broader universe of blockchain-tracked RWAs may exceed USD 5 trillion. Some more optimistic projections even point to a market of USD 30 trillion by 2033.

- Derivatives penetration: Trading volume in RWA perpetual contracts as TradFi has increased fortyfold over the past six months. This reflects strong demand for 24/7 macro exposure on-chain, especially in commodities such as gold and oil.

- Yield advantage: In the first quarter of 2026, tokenized U.S. Treasuries offered yields above DeFi stablecoin lending benchmark rates on 98% of trading days. Their volatility was also 3.6 times lower than that of native DeFi lending rates, making them a new safe harbor for on-chain capital.

From the Experimental Stage to the Mainstream Equity Market

The tokenization path for real-world assets began with highly standardized instruments such as government bonds and money market funds. Franklin Templeton’s Benji platform, launched in 2021, was one of the earliest pioneers in this field and has now operated steadily for more than five years. The real turning point, however, came when tokenization moved beyond fixed income and entered the equity market, where liquidity demand is much higher. When Robinhood announced in 2025 that it would offer more than 200 tokenized U.S. stocks to customers in the European Union, it marked the moment when tokenization entered the view of mainstream retail investors. Soon after, Kraken’s xStocks generated USD 3.6 billion in on-chain trading volume within just nine months, proving that investor acceptance of the wallet-as-account model is rising quickly.

Robinhood chief executive officer Vlad Tenev noted that “tokenization is like a freight train. It can’t be stopped, and eventually it’s going to eat the entire financial system.” - This has become one of the most representative expressions of today’s financial consensus around RWA.

A New Regulatory Blueprint: Dubai Vara Guidance and Emerging Global Compliance Standards

Regulatory progress is a prerequisite for large-scale RWA adoption. In April 2026, Dubai’s Virtual Assets Regulatory Authority, or VARA, released detailed guidance on token issuance. This set a new benchmark for the global RWA market. Rather than forcing tokens into traditional securities law, VARA created a classification system specifically designed for virtual assets.

This framework divides token issuance into three categories. Each category aligns with a different level of asset risk, while placing stronger disclosure and governance requirements on stablecoins and RWA tokens.

- Three issuance categories: The first category covers fiat-referenced assets. The second requires distribution through authorized intermediaries. The third includes exempt assets with restricted functionality.

- Disclosure transparency: Issuers must provide a detailed white paper and a separate risk disclosure statement, ensuring that reserve conditions, redemption rights, and legal structure are clear and accessible to investors.

- Compliance accountability: VARA clearly defines the due diligence obligations of licensed distributors in token issuance. This type of regulation, built specifically around the characteristics of virtual assets, offers investors more targeted protection than general legacy legal frameworks.

VARA Guidance on VA Issuance. Source: VARA

The Three Tokenization Spectrum and the Legal Boundary of Each Model

To truly understand how RWA tokenization is reshaping finance, it is not enough to say that assets are simply being brought on-chain. Based on the degree of coupling between the asset and its underlying ledger, the strength of legal protection, and the logic of technical implementation, the current market is mainly built around three distinct models. Each one comes with its own trade-off between liquidity and capital efficiency.

1. Digitally Native Tokens

This is the most complete form of tokenization. In this model, the asset exists as a digital token on the blockchain from the very beginning.

- Structure: The on-chain ledger is the single source of truth for ownership. There is no off-chain legacy system and no parallel physical record.

- Advantage: It enables true atomic settlement. Once a transaction is verified, the asset and the payment are exchanged instantly and simultaneously. This removes the multi-day settlement risk and reconciliation costs that still define traditional finance.

- User case: Franklin Templeton’s tokenized money market fund, where yield distribution is executed directly on-chain through smart contracts.

2. Synthetic Exposure Tokens

These products do not directly grant investors ownership of the underlying asset. Instead, they use a legal structure, such as an SPV, to wrap the economic return of the asset.

- Structure: The token holder owns a share in the SPV, while the SPV holds the actual stock or bond. This functions more like a swap arrangement that passes the economic benefit of an off-chain asset, such as dividends or price appreciation, into an on-chain format.

- Advantage: Because of their more permissionless design, these tokens can more easily enter DEX liquidity pools or serve as collateral in DeFi lending protocols.

- User case: Tokenized equities from Ondo Finance and Robinhood.

3. Digital Twin Tokens

This is currently the transitional model adopted by many traditional financial institutions.

- Structure: Ownership of the asset remains recorded in a traditional off-chain system, such as the DTCC ledger. The on-chain token only serves as a digital receipt or mirrored representation.

- Limitation: Token minting and burning must remain tied to the operating hours and settlement cycle of the off-chain system, such as T+1 or T+2.

- Utility: While less liquid, this model offers a high degree of transparency. Investors can use a wallet to view their holdings in traditional financial institutions in real time.

The Battleground Between Permissioned and Permissionless Systems

Once the asset model is understood, the next step is to evaluate how that asset can function within a broader ecosystem. For synthetic exposure models, the greatest attraction lies in composability. Because these tokens are generally designed to be permissionless, holders can deploy them into protocols such as Aave or MakerDAO as collateral and access leveraged strategies around the clock. This comes at a cost. Investors usually give up direct shareholder voting rights, but in return, they gain maximum capital efficiency.

By contrast, digitally native assets and digital twin assets are usually permissioned. This means that not only must the wallet address be clean, but the holder must also complete strict identity verification. That limits their use in public DeFi environments, but it opens the door to institution-grade block trading. Digitally native assets can even support second-level accruals. Interest grows continuously and is reflected directly in wallet balances. No traditional banking system can replicate that kind of experience.

The Ultimate Convergence of Financial Infrastructure: The Wallet as the Core Interface

The rise of RWA tokenization is pushing traditional finance, or TradFi, and crypto-native finance toward a shared infrastructure layer. This convergence is not accidental. It is the result of efficiency-driven change. As smart contract technology matures, many cumbersome operational processes, such as tax withholding, dividend distribution, and proxy voting, can be embedded directly into token code. This means future assets will no longer be static bookkeeping entries. They will become intelligent assets with native self-executing capabilities.

TradFi can be understood as a financial narrative that gradually emerged as real-world assets entered the crypto market. It is not the same as RWA itself. Rather, it is an extension of the trading layer built on top of RWA, tokenized equities, commodity price-linked assets, and on-chain derivatives. If RWA addresses how real-world assets are brought on-chain and digitally represented, then TradFi is about how those assets are traded at high frequency, priced in real time, leveraged, and allocated across markets once they are on-chain. This model allows traditional financial instruments such as equities, government bonds, crude oil, natural gas, and precious metals to move beyond the time constraints and geographic limits of traditional exchanges. Instead, they are repackaged and circulated through the crypto market’s familiar matching logic, margin system, and 24/7 trading framework. From this perspective, TradFi is not a simple migration of TradFi. It is a new financial interface that transforms traditional financial assets into instruments with greater liquidity, stronger tradability, and a structure more aligned with on-chain markets.

Recent TradFi-related perpetual contracts listed on the FameEX platform show that trading in the crypto market is expanding beyond native crypto narratives and moving into real-world sectors such as equities, energy, and commodities. NATGAS represents exposure to natural gas prices, with value driven by energy supply and demand, geopolitics, and the rising electricity needs of AI data centers. CL and BZ track WTI crude oil and Brent crude oil, giving users digital trading tools connected to fluctuations in global energy prices. XPT is anchored to platinum prices and brings both industrial demand and safe-haven characteristics into the on-chain asset allocation landscape. On the equity side, SNDK, MSFT, AAPL, NVDA, INTC, AMZN, and CRCL correspond to key sectors including memory chips, cloud AI, consumer technology ecosystems, AI compute, semiconductor manufacturing, cloud commerce, and stablecoin financial infrastructure. These contracts allow traditional equity value to enter a 24-hour trading environment through USDT-margined perpetual futures. These RWA perpetual contracts together are not simply an extension of product variety. They convert corporate cash flows, energy pricing, and commodity supply-demand cycles from the real economy into cross-market instruments that can be priced, hedged, and allocated inside the crypto market. To stay aligned with the RWA market trend, explore the related contract trading gateways below:

- NATGAS/USDT Futures Trading: https://www.fameex.com/en-US/swap/E-NATGAS-USDT

- CL/USDT Futures Trading: https://www.fameex.com/en-US/swap/E-CL-USDT

- BZ/USDT Futures Trading: https://www.fameex.com/en-US/swap/E-BZ-USDT

- XPT/USDT Futures Trading: https://www.fameex.com/en-US/swap/E-XPT-USDT

- SNDK/USDT Futures Trading: https://www.fameex.com/en-US/swap/E-SNDK-USDT

- MSFT/USDT Futures Trading: https://www.fameex.com/en-US/swap/E-MSFT-USDT

- AAPL/USDT Futures Trading: https://www.fameex.com/en-US/swap/E-AAPL-USDT

- NVDA/USDT Futures Trading: https://www.fameex.com/en-US/swap/E-NVDA-USDT

- INTC/USDT Futures Trading: https://www.fameex.com/en-US/swap/E-INTC-USDT

- AMZN/USDT Futures Trading: https://www.fameex.com/en-US/swap/E-AMZN-USDT

- CRCL/USDT Futures Trading: https://www.fameex.com/en-US/swap/E-CRCL-USDT

Conclusion

Based on the current direction of development, RWA tokenization is not merely about moving traditional assets onto blockchain rails. It is a foundational revolution in financial infrastructure. Through the overlapping evolution of digitally native assets, synthetic exposure, and digital twin models, we are witnessing capital movement compress from days to seconds, and financial records shift from closed ledgers to transparent on-chain books. As financial giants and crypto-native protocols converge on the same infrastructure, the boundary around assets will be fundamentally dissolved. In the future, the wallet will become the only real financial passport, while RWAs will serve as the bridge that leads USD 30 trillion in assets into a new financial era that is always on, programmable, and highly efficient.

FAQ

Q1: Are Tokenized RWA Products, Such as Tokenized U.S. Equities, Legally Protected for Investors?

That depends on the asset model. Digitally native and digital twin models usually operate within regulated frameworks, where investors have direct or clearly documented legal ownership. Synthetic exposure models, by contrast, depend on the contractual credibility of the issuer, such as an SPV. Before participating, investors should carefully review the legal structure and whitepaper of the product.

Q2: Can On-chain RWA Products De-peg From Their Off-chain Reference Price?

Yes, that is possible. This is especially true for synthetic assets and for tokens that trade actively in secondary markets. If on-chain liquidity is weak, or if the off-chain underlying asset faces redemption or settlement stress, token prices may diverge from the value of the actual asset. For more mature digitally native products, however, market makers and arbitrage mechanisms are often in place to help keep the token price aligned with the underlying asset.

Q3: Compared With Holding Assets Through a Traditional Broker, What Costs Do Tokenized Assets Actually Reduce?

The most direct savings come from reconciliation and settlement. Traditional trading requires data matching across brokers, clearing houses, custodians, and other intermediaries. That is also why settlement still takes T+2 in many markets. The blockchain ledger itself serves as the single source of truth and allows real-time settlement. This removes a large share of intermediary fees and administrative costs, while also reducing the opportunity cost of capital locked during the settlement window.

Disclaimer: The information provided in this article is intended only for educational and reference purposes and should not be considered investment advice. Conduct your own research and seek advice from a professional financial advisor before making any investment decisions. FameEX is not liable for any direct or indirect losses incurred from the use of or reliance on the information in this article.