Research

FameEX Research focuses on the digital asset industry, providing expert analysis and objective reporting for global participants, with a commitment to original content and global connections.

Industry Analysis

- Heurist Deep Research positions itself as a Web3-native research assistant that can orchestrate multiple AI services; the pay-per-use model aligns naturally with x402.

- Daydreams has experimented with x402 to support per-generation or per-task inference workflows for LLMs.

- Firecrawl exposes web search/scrape and cleaning APIs and has showcased per-call access patterns that map well to x402’s pay-per-request model.

- Performance trade-offs: Early implementations can involve multiple network interactions (challenge, verification, settlement), leading to end-to-end latencies in the hundreds of milliseconds per paid request. When an AI agent accesses many paid resources in parallel, those costs can compound and degrade user experience. Roadmaps for a v2 flow focus on reducing round-trip and optimizing the transport layer, but larger gains may also require architectural techniques such as batching, short-lived entitlements, or deferred settlement.

- Facilitator incentives: Many deployments rely on facilitators/relays to verify authorizations and, where needed, submit transactions on-chain. While this simplifies integration, it raises questions about fee models, incentives, and potential centralization. Long-term sustainability will depend on clear pricing, competition among facilitators, and transparent service guarantees.

- Token and standard support: In current practice, x402 most commonly uses USDC with EIP-3009 to enable gasless authorizations. Broader asset coverage (for example, ERC-2612 Permit flows and additional stablecoins) depends on token contract capabilities and ecosystem tooling. It is more accurate to say today’s implementations center on EIP-3009-compatible assets rather than strictly mandate them. For example, Tether—the issuer of USDT—has not made any public, primary statements confirming long-term support for EIP-3009.

- Regulatory considerations: x402 is a protocol; compliance obligations rest with implementers (merchants, facilitators, and wallets). Global rollouts must align with KYC/AML and payment rules that differ by jurisdiction. Frameworks such as the EU’s MiCA and evolving U.S. guidance on digital assets indicate that regulatory treatment is still developing and may impose licensing, reporting, and consumer-protection requirements on services that use x402.

How Base MCP Turns AI Agents into Web3 Asset Assistants

The RWA Tokenization Boom in 7 Charts

2026 RWA Tokenization Trends and the Rise of TradFi

From DeFi Automation to AgentFi Intelligence: The Next Era of On-Chain Asset Management

AgentFi is turning DeFi from manual strategy juggling into AI-driven, 24/7 asset management. We unpack its tech stack, core use cases, risks, and the path toward multi-agent financial networks.

What is the x402 Protocol? A New Standard Reshaping Internet Payment Protocol

Key Highlights

The x402 protocol is a new web-native payment standard built on HTTP/1.1’s long-reserved 402 “Payment Required” status code. Coinbase introduced x402 on May 6, 2025, and on September 23, 2025, Coinbase and Cloudflare announced the x402 Foundation to steward the open standard. The protocol is designed to automate micropayments for online resources using blockchain settlement, typically stablecoins such as USDC.

Amid the rapid development of the AI-agent economy, x402 provides the technical foundation for value exchange between machines. Its core value lies in embedding payment directly into the web protocol stack, opening new possibilities for Internet business models. This article examines x402 across five dimensions: technological evolution, project principles, application ecosystem, advantages and challenges, and development outlook.

The Origins of the x402 Protocol: From a Reserved Status Protocol to Commercial Applications

The x402 protocol traces its roots to the HTTP/1.1 specification published in 1997 (RFC 2068), which first defined status code 402 “Payment Required.” Importantly, the spec marked 402 as “reserved for future use,” and it saw little real-world adoption for decades due to the lack of reliable micropayment rails. This long-standing reservation reflected early designers’ foresight about web commercialization, while also highlighting a timing gap between technical feasibility and business needs.

Over the past two decades, the Internet’s business models have centered on advertising and subscriptions. Industry data indicates that global ad spending reached around US$1.1 trillion in 2024, with digital channels accounting for the majority; estimates for the subscription economy vary by methodology but place it in the hundreds of billions of dollars and growing. These models scaled access to online services, yet introduced structural issues such as privacy trade-offs, content homogenization, and uneven creator compensation. The x402 protocol provides a technical path to explore finer-grained, per-use pricing.

By 2025, improvements in blockchain infrastructure, the maturation of stablecoins, and the rise of the AI-agent economy converged to make per-request payments practical. Coinbase introduced x402 on May 6, 2025, and in September 2025, Coinbase and Cloudflare announced the x402 Foundation to steward the open standard—turning a long-reserved HTTP status into working plumbing for value exchange on the web. This marks a meaningful step in the evolution of Internet protocols from pure information transport toward value transfer.

Technical Principles of the x402 Protocol: A Blockchain-Backed Payment Integration Framework

The x402 payment flow is intentionally simple. When a client requests a resource, the server responds with HTTP 402 (Payment Required) to trigger payment. That response includes a machine-readable invoice—amount, accepted currency (often a stablecoin), destination, and other network parameters. The client then authorizes the payment in a compatible wallet and retries the same request with a signed payment payload attached in a payment header. If the server (or a facilitator acting on its behalf) verifies the authorization, it returns the resource. In short: Request → 402 with terms → Authorized retry → Access—a flow that avoids traditional web payment friction (create account, link your card, or fill in more details) and stays faithful to HTTP’s native semantics.

At the settlement layer, the reference v1 design commonly uses EIP-3009 transferWithAuthorization, which lets users sign an off-chain authorization that a facilitator can submit on-chain. This yields two key benefits:

(1) A “gasless” experience for end users (they don’t need to hold the chain’s native token)

(2) Strong safety properties via nonces and validity windows that provide replay protection.

Crucially, x402 employs a facilitator (relay) architecture to make large-scale commercial adoption practical. Facilitators handle verification, blockchain interaction/settlement, and simple APIs that resource servers call during the 402 → paid-retry cycle—significantly lowering integration complexity. In production, facilitators typically support USDC and other EIP-3009-compatible tokens on supported networks (e.g., Base), with broader token and network support expanding over time.

For cryptographic assurances, implementations use standard ECDSA-based signatures (EIP-712 typed data) so that payment authorizations are non-repudiable. Each payment carries anti-replay parameters—nonces, timestamps, and expiration windows—that are validated before access is granted. This preserves blockchain-level trust while meeting web-scale needs for low latency and high throughput.

Application Usages of the x402 Protocol: Multi-Scenario Adoption from the AI Economy to Digital Content

According to industry analyses from Gartner, machine customers—autonomous AI agents that buy goods and services—are expected to drive trillions of dollars in purchases and account for roughly 15–20% of revenue for many enterprises by 2030. This makes the AI-agent economy a natural fit for x402. The protocol provides a machine-native way for agents to pay per request, enabling AI systems to acquire training data, call APIs, and rent compute resources autonomously. For example, a research-oriented agent could use x402 to purchase time-boxed access to a specialist database and iteratively improve its models.

In today’s API markets, prepaid and postpaid subscriptions often misalign with granular usage and inhibit long-tail demand. By contrast, x402 supports pay-per-use with metering and settlement embedded in the HTTP flow. Early experiments from data and tooling providers illustrate how providers can price precisely at the request level and settle instantly, such as Firecrawl exposing per-call search/scrape endpoints via x402. This reduces friction for small and high-frequency transactions.

For digital media and creators, x402 offers a direct micropayment path that complements or substitutes for ads and bundles. Projects like Gloria AI have explored pay-per-article access using x402, while platforms such as tip.md platform integrate agent workflows so an AI assistant can tip on a user’s behalf. These pilots point toward new value-sharing models in human–machine collaboration, even as the broader ecosystem is still in an early, experimental phase.

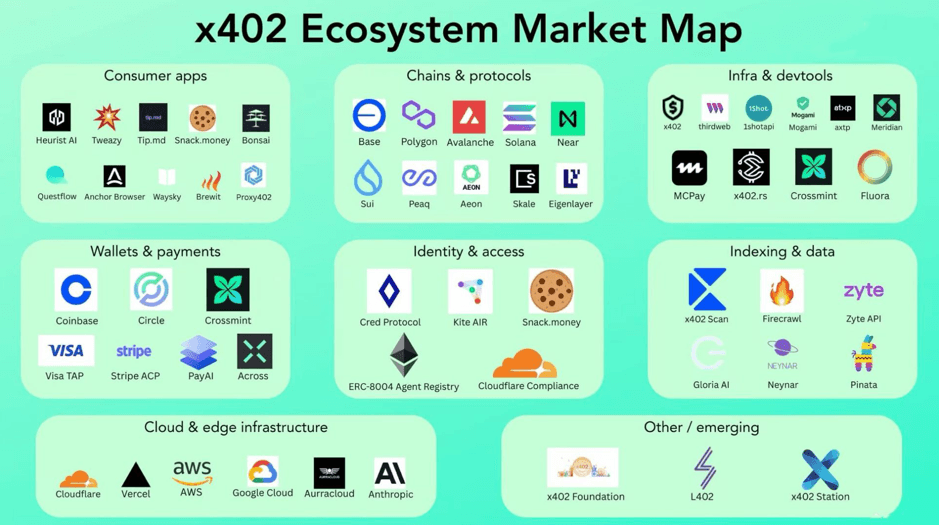

Ecosystem Applications of the x402 Protocol: An Emerging Contender with Strong Potential

Since its introduction, the x402 protocol’s straightforward payment flow and broad applicability have attracted early interest across several layers of the stack—protocols and standards, infrastructure, core applications, and cloud services. The emerging ecosystem market map shows promising momentum for x402 as a next-generation payment rail. While it’s still early, the combination of HTTP-native design, stablecoin settlement, and agent-friendly workflows positions x402 as a credible contender to power pay-per-use experiences across APIs, data, and digital content.

x402 Ecosystem Market Map

1) Protocols & Standards Layer

This layer defines the “grammar” of the x402 ecosystem so AI agents can understand one another and transact. When paired with complementary agent standards, x402 opens a new path for web payments. For example, Google’s A2A initiatives focus on standardizing agent-to-agent communication; Anthropic’s MCP helps agents securely access tools and data; and Google’s AP2 (Agent Payments Protocol) targets on-demand service invocation and automated payments. Together with x402—which gives concrete meaning to HTTP 402—these efforts point toward interoperable, machine-native commerce.

2) Infrastructure Layer

If x402 defines “what” to do, infrastructure is “how” to do it. In practice, this includes facilitators/relays that verify payment authorizations and, when needed, submit settlements on-chain, plus SDKs and gateways that simplify server integrations. Services such as PayAI position themselves as multi-chain coordinators that help developers and agents validate payments and complete settlement with low latency—akin to “Stripe” or “Alipay” service.

In parallel, some blockchain projects are exploring native support for x402-style payments. For example, Kite AI is described as a Layer-1 focused on agent transactions, while Peaq targets the broader machine economy (DePIN), aiming to enable device-to-device automated payments. These efforts are early, but they illustrate how settlement layers may evolve to serve agent workloads.

3) Core Application Layer

This is where users and agents encounter real “products” and “services.” Here are several examples below:

Together, these examples demonstrate how metered APIs, agent tools, and research/inference pipelines can adopt x402 for precise, transaction-level pricing.

4) Cloud Services

Major network and cloud providers are beginning to surface x402 in developer tooling and edge workflows. Coinbase and Cloudflare have announced this collaboration via the x402 Foundation to steward the open standard and support integrations. As those integrations mature, global distribution and edge verification can reduce latency and make per-request payments more practical at scale.

x402 Protocol Ecosystem Map

Competition and Challenges of the x402 Protocol: A Delicate Balance Between Technical Features and Commercial Applications

From both business and engineering perspectives, x402’s advantages fall into three categories. First, it reduces the economics of micropayments relative to traditional card rails. Second, it fits naturally into existing HTTP workflows, lowering integration overhead. Third, it natively supports automated, agent-driven transactions. Here are more details below.

1. Economic efficiency: Per-request settlement over stablecoin rails can be materially cheaper than traditional card networks (typically 2–3%), making true micropayments more viable.

2. Technical compatibility: Because x402 repurposes the standard HTTP 402 “Payment Required” status, it integrates cleanly with existing web infrastructure and developer workflows, which lowers merchant onboarding costs.

3. Automation: The protocol enables direct machine-to-machine value exchange without account creation, card binding, or form filling—laying essential groundwork for autonomous economic activity.

However, x402 still faces several challenges going forward:

Development Outlook for the x402 Protocol: From Technical Experimentation to Ecosystem Building

Based on public roadmaps and community discussions, a forthcoming v2 direction for x402 emphasizes three areas: (1) transport-layer abstraction so payments can attach to multiple communication patterns beyond basic HTTP; (2) greater scheme extensibility to allow custom payment logic and authorization methods; and (3) service-discovery mechanisms to simplify client configuration. While these improvements do not fully resolve foundational questions—such as long-term incentives for facilitators—they meaningfully increase the protocol’s practicality and flexibility.

The x402 ecosystem is still in the early transition from technical validation to broader commercial rollout. Developer activity and community interest are rising, but production deployments remain limited. Achieving network effects will likely require more “flagship” applications—such as Daydreams or Heurist Deep Research—to demonstrate clear commercial value and pull in upstream and downstream partners and investors.

From a go-to-market perspective, x402 faces a two-sided learning curve. Traditional web developers need approachable tooling and guidance for blockchain settlement, while the crypto community must adapt to conventional web-protocol paradigms—complete documentation, robust SDKs, and a growing catalog of case studies.

In the longer term, the x402 protocol value may concentrate in three areas: (1) Base settlement infrastructure (e.g., Base, Solana) benefiting from increased transaction flow as adoption grows; (2) Payment aggregators and facilitators (e.g., PayAI) emerging as key nodes that abstract multiple chains and tokens; and (3) Vertical solutions (e.g., Daydreams) achieving early product-market fit with pay-per-use models. Investors should focus on teams with technical defensibility and strong ecosystem integration, while carefully weighing technical risks and policy uncertainty as the protocol evolves.

From technical standard to business practice, x402 represents a significant step in the evolution of the Internet’s value. It revives a long-reserved HTTP status code and supplies payment infrastructure for human-machine collaboration and machine autonomy in the AI economy. Although challenges remain in performance at scale, facilitator economics, and compliance, x402’s technical direction and ecosystem openness position it as a credible component of the next-generation Internet architecture. As iteration continues and the ecosystem matures, x402 could play a meaningful role in reshaping how value is exchanged online.

Project Report

NFLX (Netflix) Token Price & Latest Live Chart

Discover the latest NFLX price with FameEX's NFLX/AUD Price Index and Live Chart. Keep up-to-date with the current market value and 24-hour changes, as well as delve into Netflix's price history. Start tracking NFLX price today!

UBER (Uber) Token Price & Latest Live Chart

Discover the latest UBER price with FameEX's UBER/AUD Price Index and Live Chart. Keep up-to-date with the current market value and 24-hour changes, as well as delve into Uber's price history. Start tracking UBER price today!

AMD (Advanced Micro Devices) Token Price & Latest Live Chart

Discover the latest AMD price with FameEX's AMD/AUD Price Index and Live Chart. Keep up-to-date with the current market value and 24-hour changes, as well as delve into Advanced Micro Devices's price history. Start tracking AMD price today!

SAMSUNG (Samsung Electronics Co., Ltd) Token Price & Latest Live Chart

Discover the latest SAMSUNG price with FameEX's SAMSUNG/AUD Price Index and Live Chart. Keep up-to-date with the current market value and 24-hour changes, as well as delve into Samsung Electronics Co., Ltd's price history. Start tracking SAMSUNG price today!

OPENAI (OpenAI Group PBC) Token Price & Latest Live Chart

Discover the latest OPENAI price with FameEX's OPENAI/AUD Price Index and Live Chart. Keep up-to-date with the current market value and 24-hour changes, as well as delve into OpenAI Group PBC's price history. Start tracking OPENAI price today!