BSB (Block Street) Token Price & Latest Live Chart

2026-05-21 11:04:14

What is BSB (Block Street)?

BSB is the native token of the Block Street ecosystem, while Block Street itself is a liquidity infrastructure protocol built for tokenized assets and on-chain capital markets. It is not simply a trading platform, nor is it an RWA protocol that serves only one asset issuer. Instead, it aims to establish a unified liquidity network across different chains, issuers, and trading venues. As equities, bonds, ETFs, commodities, and other real-world assets gradually enter blockchain networks in tokenized form, the core market question is no longer limited to how these assets can be brought on-chain. The more important question is whether these on-chain assets can be traded, collateralized, borrowed against, and used in composable strategies with sufficient efficiency. Block Street is positioned to address this layer of market infrastructure. Its goal is to prevent tokenized assets from remaining fragmented across isolated trading pools, single issuers, or individual chains. Through a unified liquidity layer, these assets can enter a deeper and more composable on-chain capital market.

Source: https://x.com/BlockSt_HQ

Block Street addresses the fragmentation pain point within tokenized asset markets. When traditional financial assets move on-chain, liquidity often becomes separated across different issuers, compliance frameworks, blockchain environments, and trading venues. A tokenized equity may have one version on Ethereum and another version on BNB Chain. It may also be wrapped or issued in different formats by different providers. Although these assets may track similar underlying instruments, their trading depth, quote efficiency, and settlement processes remain disconnected. This leaves users facing higher slippage, wider bid-ask spreads, and weaker capital efficiency. Block Street connects these fragmented markets through a unified liquidity layer, allowing quotation, matching, collateralization, and settlement to operate within the same infrastructure stack. This helps reduce friction costs across the tokenized asset market.

In addition, Block Street combines the asset depth of TradeFi with the composability of DeFi. Traditional financial markets have massive asset scale and mature risk management models, but they are also constrained by market hours, longer settlement cycles, geographic access barriers, and complex intermediary structures. DeFi offers 24/7 trading, composability, real-time settlement, and open global access. However, tokenized equities and RWA assets still lack sufficiently deep trading and financing infrastructure on-chain. Block Street attempts to build a bridge between these two systems. It allows tokenized assets to exist not only as passive on-chain representations, but also as instruments that can be used for collateral, lending, routed execution, and cross-protocol strategies in a way that resembles crypto-native assets. This is the core direction represented by BSB, which is to support a scalable on-chain financial infrastructure around tokenized capital markets.

At the level of technical strength and institutional background, the project has a strong institutional background and deep technical foundation. Its founding team brings together Wall Street quantitative finance experience and top-tier Silicon Valley distributed systems engineering expertise. Team members have previously worked at leading traditional quantitative trading and financial institutions, including Citadel Securities, Point72 Asset Management, Jane Street, and Hudson River Trading. This background gives the project a Wall Street-grade execution mindset and risk architecture from its earliest design stage. During its early testnet phase, the project showed strong market attention and attracted as many as 700,000 testnet wallets. This infrastructure has also received ecosystem support from public chains including BNB Chain and has formed deep strategic collaborations with multiple real-world asset issuers and decentralized finance infrastructure providers. Together, these partnerships aim to advance the broader transformation of on-chain capital markets.

How does BSB (Block Street) work?

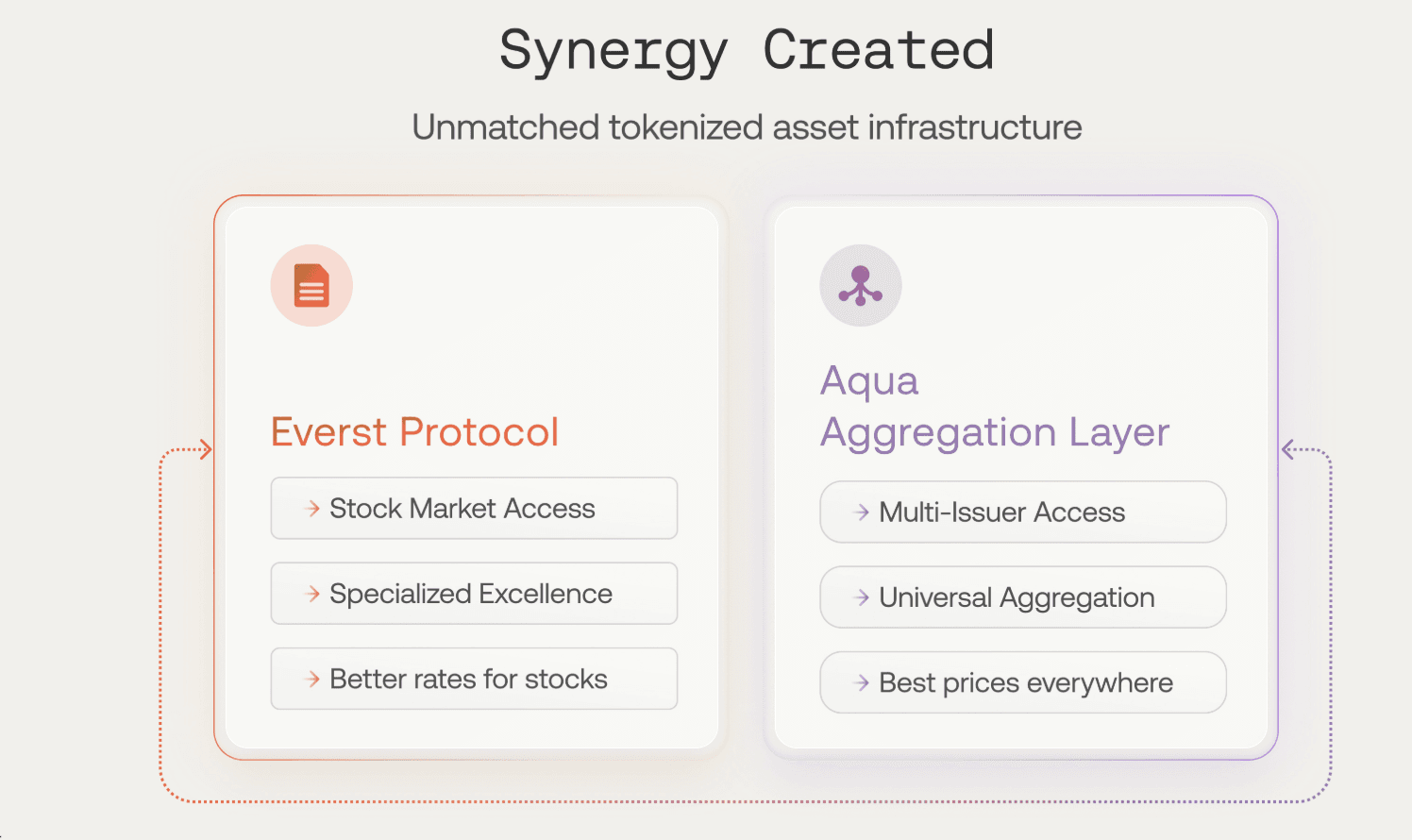

Block Street’s operating core is mainly built around two products and one governance staking system. Aqua handles liquidity flow and trade execution, Everst handles leverage, lending, and capital efficiency, while BlockStreet Staking turns BSB holdings into governance participation and staking weight. Aqua functions more like a cross-protocol liquidity network and execution layer, while Everst is closer to the capital efficiency layer for tokenized assets. When these two products work together, Block Street does more than provide a buying and selling channel. It allows tokenized assets to move through a fuller market cycle that includes trading, financing, collateralization, and strategy composition. Aqua is the core module through which Block Street addresses liquidity fragmentation. It is a cross-protocol liquidity network that uses RFQ quotes, WebSocket access, cross-chain routing, and multi-source liquidity aggregation to provide a more efficient execution environment for tokenized assets. Traditional AMM models are highly suitable for crypto-native tokens, but when they face equities, ETFs, bonds, and other assets with clear off-chain price anchors, pure AMMs can suffer from poor capital efficiency and wider slippage. Aqua adopts an RFQ execution model that is closer to institutional trading. It sources quotes from market makers, institutional trading desks, and on-chain liquidity pools, then finds a more suitable execution path for each order. This model means tokenized asset trading no longer depends entirely on passive liquidity pools. Instead, it can access more flexible quoting and a trading mechanism closer to professional markets.

Everst Protocol and Aqua aggregation layer synergy, source: https://docs.blockstreet.money/docs

Everst is Block Street’s leverage and liquidity protocol. Its main function is to allow tokenized assets to be borrowed, collateralized, and reused. For tokenized equities or ETFs, if the assets can only be bought and sold, the market remains at a basic trading layer. Everst brings these assets into DeFi’s capital efficiency system, allowing them to function as collateral, lending assets, or components of leveraged strategies. Everst also supports major TradeFi assets such as AAPL, TSLA, and NVDA, as well as ETFs such as SPY and QQQ. Through the Hybrid Liquidity Engine, it connects off-chain broker-dealer networks with on-chain liquidity pools. This design allows Everst to benefit from off-chain quotation and execution efficiency while preserving on-chain settlement, transparency, and composability. The project’s proprietary hybrid liquidity engine and multi-layer security risk control model combine the high execution efficiency of off-chain brokerage networks with the advantages of decentralized on-chain settlement. It also introduces EIP-712 cryptographic signatures to strictly verify each RFQ quote on-chain. For dynamic risk management, the system supports cross-protocol collateral movement and real-time risk netting. It can dynamically adjust loan-to-value ratios based on market volatility, helping maintain institutional-grade asset security and compliance. These combined mechanisms mean tokenized assets do not merely exist on-chain. They can operate within a framework that is closer to institutional market standards, which also marks a key difference between Block Street and a standard DEX or single-issuer RWA platform.

BSB (Block Street) market price & tokenomics

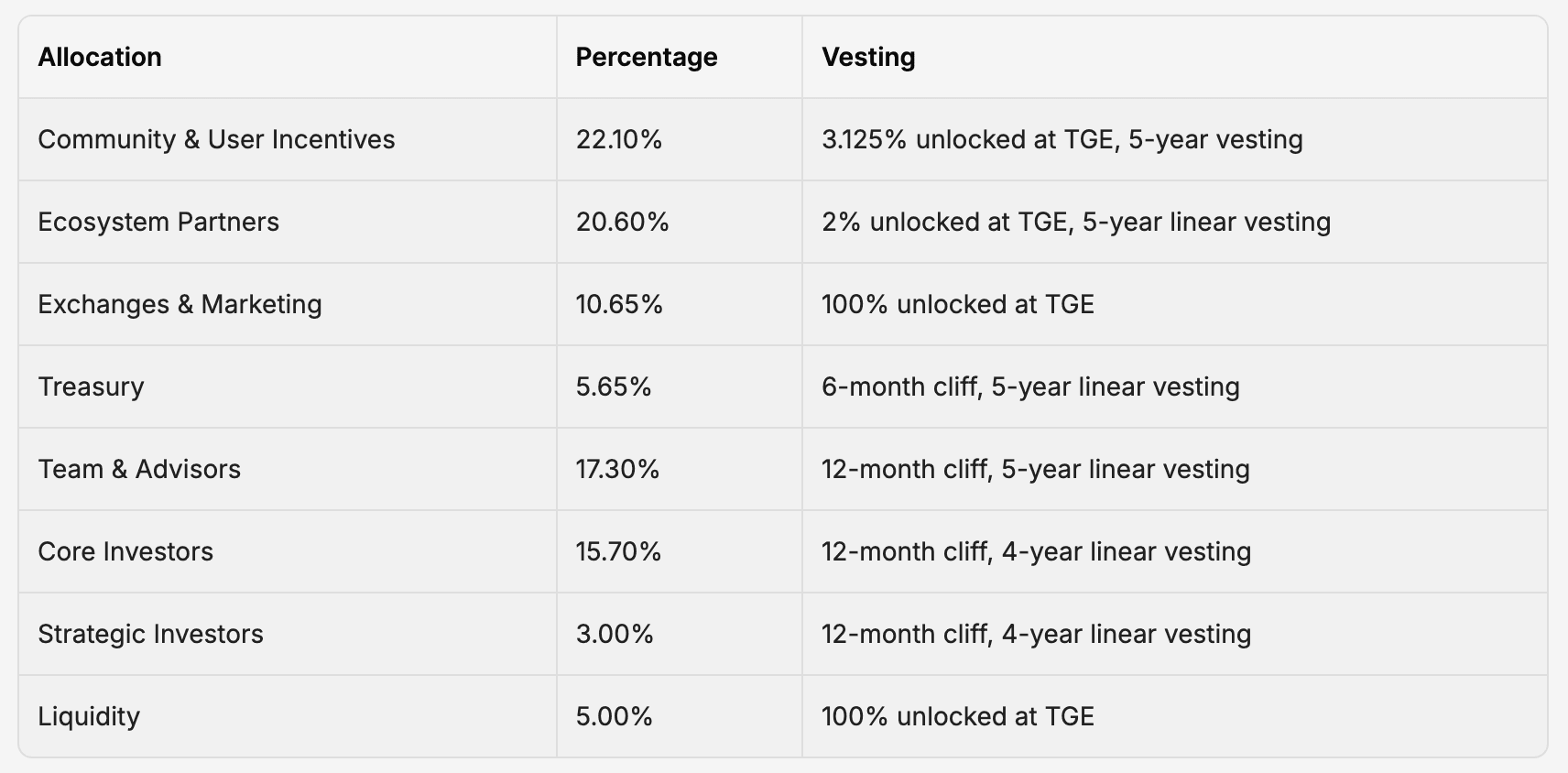

As the equity and governance core of the entire infrastructure ecosystem, the BSB token is designed with rigorous utility integration and long-term supply discipline. Its maximum total supply is 1,000,000,000 tokens. The token adopts a multi-chain issuance model and exists both as an ERC-20 token on Ethereum and a BEP-20 token on BNB Smart Chain. It officially launched its Token Generation Event on March 4, 2026, followed by listings on several major centralized exchanges. At the initial token release, around 20.775% of the total supply entered market circulation, while the remaining allocation was assigned to long-term incentive plans. The project designed a staged release structure with lockups and linear vesting for different stakeholder groups. Community and user incentives account for 22.1%, ecosystem partners receive 20.6%, core investors, strategic investors, and team and advisors receive 15.7%, 3%, and 17.3%, respectively. Exchanges and marketing account for 10.65%, liquidity seed capital accounts for 5%, and the remaining 5.65% is allocated to treasury reserves. This structure is intended to align token supply growth with actual platform adoption while reducing excessive early-stage selling pressure.

$BSB token allocation, Source: https://docs.blockstreet.money/docs/whitepaper

At the protocol utility level, BSB plays an essential role as the economic engine of the ecosystem, mainly across five core areas. First is governance. Token holders can vote on the platform’s fee structure, risk parameters, treasury allocation, and the onboarding of new assets. Second, users who hold the token can receive meaningful trading fee reductions across the Aqua and Everst protocols. Third, the token can be used directly as eligible collateral inside the Everst lending protocol, allowing holders to borrow other tokenized equities without selling their BSB. Fourth is the staking and revenue sharing mechanism. Part of the trading fees generated by the platform may be used for buybacks and then distributed to stakers or burned. Finally, token holders may gain exclusive priority API access and the right to participate in liquidation auctions within Everst. This creates practical incentives for advanced traders and institutional participants.

BlockStreet Staking turns BSB from a simple holding asset into a governance participation tool. Its staking model uses a single shared lock pool, where all staking positions share one global unlock date. The unlock time is 365 days after the program launch, and early withdrawal is not supported before that global unlock date. A staker’s voting weight increases linearly with staking time, starting from 1x and gradually rising to a maximum of 4x after 365 days. Eligible stakers with at least 100,000 BSB staked can submit proposals containing a title and an IPFS link. These proposals do not need to be tied to one fixed voting cycle. Block Street later selects proposals for a specific epoch, sets the voting duration and reward amount, then opens voting. Users can vote YES or NO on proposals. Both directions represent governance signals, but they do not affect reward eligibility. Rewards come from voting participation itself. If one address votes on multiple proposals within the same epoch, the reward calculation only uses the highest single voting weight reached by that address in that epoch. Ultimately, the project aims to build a base-layer capital market network that supports trading, lending, leverage, governance, liquidity routing, and institutional-grade access.

Why do you invest in BSB (Block Street)?

The pain point in on-chain capital markets lies in the lack of a standardized clearing and settlement layer. Block Street addresses this structural demand by providing a unified liquidity pipeline. As more tokenized asset issuers join the network, the depth aggregated by the platform can increase, which may then attract more DeFi applications and traders. Once this self-reinforcing cycle takes shape, it can create a strong competitive moat in the tokenized securities market. The project has already captured more than 65% institutional market share across integrated venues, reached $118,000,000 USD in blended monthly volume, and surpassed $241,000,000 USD in cumulative transaction volume. These figures show that its product-market fit has already received validation from real capital activity.

In 2026, real-world assets and tokenized equities have become core themes in the crypto market. Asset tokenization only completes the first stage of development. When large volumes of equities, ETFs, bonds, and yield-bearing assets begin circulating on-chain in tokenized form, the ecosystem’s demand for high-quality execution, deep liquidity, mature collateral frameworks, and reliable cross-chain settlement will become significantly stronger. Block Street does not position itself as a competitor limited to issuing a single asset. Instead, it positions itself as a unified liquidity layer across different issuers, protocols, and users. This role makes it closer to the financial pipes and base architecture of on-chain markets. Its distinction also lies in the simultaneous development of two flagship products, Aqua and Everst. Aqua focuses on trade execution and cross-protocol liquidity routing, while Everst focuses on collateralized lending and leveraged capital efficiency. This two-layer architecture allows tokenized assets to move beyond simple spot trading and enter a full cycle of leverage, lending, and strategy composition. Therefore, Block Street has broader product coverage and stronger extensibility than a single trading venue or asset issuance platform. This positions it as a neutral and potentially essential aggregator in a market where liquidity fragmentation continues to intensify.

Is BSB (Block Street) a good investment?

Whether BSB is worth investing in depends on whether the protocol can turn its technical performance into long-term and resilient liquidity depth. Block Street’s product matrix combines Aqua’s RFQ execution network, Everst’s leverage and lending framework, and the Hybrid Liquidity Engine. Together, these components target structural pain points in tokenized asset markets, including capital efficiency, cross-chain settlement, and fragmented liquidity. However, investors need to distinguish carefully between technical capability and commercial viability. The project’s long-term value cannot rely on narrative alone. Its future ceiling will depend heavily on post-mainnet trading scale, real paid demand, the depth of institutional market maker participation, and the level of integration with DeFi protocols. It will also be important to observe whether Block Street can maintain quote quality, API stability, and cross-protocol risk management in real market environments.

Beyond potential upside, investors also need to examine the project’s regulatory barriers, market competition, and long-term token supply inflation. The development of tokenized equities and real-world assets involves securities regulation, cross-border financial access, issuer compliance, and on-chain settlement standards. These external regulatory conditions may directly limit the asset types that the platform can support and the speed of market expansion. On the competitive side, several protocols and traditional financial institutions have already entered on-chain capital markets with a focus on issuance, lending, or asset management. For Block Street to become the default unified liquidity layer, it must prove its quote quality, API stability, risk control capabilities, partnership depth, and cost advantages for users. A balanced conclusion is that BSB represents a high-growth but high-risk allocation to the base network of on-chain capital markets. Its total supply will continue entering the secondary market through linear unlocks over the next five years. Therefore, its evaluation should not be built on short-term price expectations. It should be based on continued tracking of trading volume, lending TVL, institutional integration, staking participation, and whether fee revenue can form a healthy positive cycle with token utility.

Explore the latest BSB (Block Street) price and live chart, trade BSB on FameEX, and access real-time market data! Get started now with a seamless trading experience!

Disclaimer: The information provided in this article is intended only for educational and reference purposes and should not be considered investment advice. Conduct your own research and seek advice from a professional financial advisor before making any investment decisions. FameEX is not liable for any direct or indirect losses incurred from the use of or reliance on the information in this article.