FameEX Crypto Market Trend | June 9, 2026

2026-06-09 12:01:40

Market expects Fed & ECB rate hikes in mid-June while renewed US-Iran conflict in the Middle East, heightening panic.

I. Core Market Overview

1. BTC Spot Performance

Price Range: 59,100.2 USD - 78,164 USD

Weekly Volatility: 32.36%

Key Driving Factors:

Primary Factors: Growing market expectations that both the Federal Reserve and the European Central Bank will raise interest rates in mid-June this year.

Secondary Factor: Renewed military conflict between the United States and Iran in the Middle East, coupled with heightened market panic sentiment.

2. Central Bank Policy Updates

Policy Impact Assessment:

Federal Reserve officials: It is increasingly evident that policymakers are leaning more hawkish, signaling rising expectations for interest rate hikes.

ECB: The focus has clearly shifted toward rate increases, with virtually no discussion of rate cuts remaining. Ahead of the upcoming policy meeting, further hikes are now largely priced in by the market.

3. Other Key Updates

Kevin Warsh, the incoming Federal Reserve Chair, was formerly an investment banker at Morgan Stanley. In 2006, he was appointed to the Federal Reserve Board by former President George W. Bush, becoming the youngest Fed governor in history at the age of 35.

During the financial crisis two years later, he played a key role in finalizing bailout measures and helping rescue major Wall Street banks from the brink of collapse. However, by the time he left the Fed in 2011, he had become a critic of its policy direction, expressing concern that continued monetary support for financial markets after the recovery had gone too far.

During Donald Trump’s first term, Warsh sought the nomination for Fed Chair but ultimately lost to Jerome Powell. During the COVID-19 pandemic, he—long known for his hawkish stance on inflation—warned ahead of time that the Fed’s aggressive support for the economy could lead to severe inflation in the future.

Since January 2012, the Fed has treated a 2% inflation target as the “gold standard” of monetary policy. This long-standing “red line,” unchanged for 14 years, has served both as a benchmark for policy performance and a cornerstone for global investor expectations. However, in Warsh’s view, this benchmark may already be outdated. In testimony before the Senate Banking Committee, he put forward a highly disruptive and subjective perspective, arguing that “price stability” should not be defined by a rigid number, but rather by a condition in which “no one is talking about price changes.” This tendency to “de-numericalize” the inflation target has raised deep concerns among markets.

On June 5, according to the official U.S. Congress website, the full text of the “American Reserve Modernization Act” (H.R.8957, ARMA) was released. The bill was introduced on May 21 by Representative Nicholas Begich of Alaska and has been referred to the House Financial Services Committee for review.

The main provisions include incorporating Bitcoin acquired by the government through criminal or civil forfeiture into a Strategic Bitcoin Reserve managed by the Treasury Department, with a minimum holding period of 20 years during which assets cannot be sold or disposed of. The bill also establishes a quarterly proof-of-reserve mechanism with independent third-party audits. It allows states to voluntarily custody their Bitcoin in separate accounts within the Federal Reserve System.

Looking forward, the bill requires the Treasury and Commerce Departments to jointly study within 180 days the feasibility of expanding Bitcoin holdings in a budget-neutral manner. Potential sources include converting non-Bitcoin digital assets, forfeited assets, voluntary donations, tax or tariff revenues, as well as mechanisms involving the Fed or gold certificates.

Additionally, any forked assets or airdrops received from government-controlled addresses must be properly safeguarded. Sale of forked or airdropped assets is prohibited for five years. After five years, their market value must be assessed: the dominant asset (highest market capitalization) must be retained, while others may be liquidated with proceeds returned to the Treasury. Assets with unique strategic value may be recommended to Congress for retention.

Analysts note that compared with the earlier BITCOIN Act, which called for the purchase of 1 million BTC, the ARMA bill is more moderate and politically feasible. However, it still leaves room for future federal expansion of Bitcoin holdings.

II. Market Health Index Analysis (Source: CoinMarketCap)

Source: https://coinmarketcap.com/charts/

Conclusion:

Market capitalization is declining, and shrinking trading volume suggests a market driven by existing capital rather than new inflows.

The altcoin season index is in the 25–55 range, indicating capital rotation back into Bitcoin. After a period of consecutive ETF outflows, flows have recently turned slightly positive again. Combined with the Fear & Greed Index sitting in extreme fear, this reflects weakening market confidence.

III. Derivatives Monitor (Source: CoinAnk)

1. Funding Rate

30-Day Avg Funding Rate of Bitcoin Across the Top Six CEXs: 0.1112% (Positive)

30-Day Avg Funding Rate of ETH Across the Top Six CEXs: -1.0127% (Negative)

Source: https://coinank.com/fundingRate/current

Interpretation:

A predominantly negative funding rate indicates that short positions are dominant in the market, reinforcing bearish expectations.

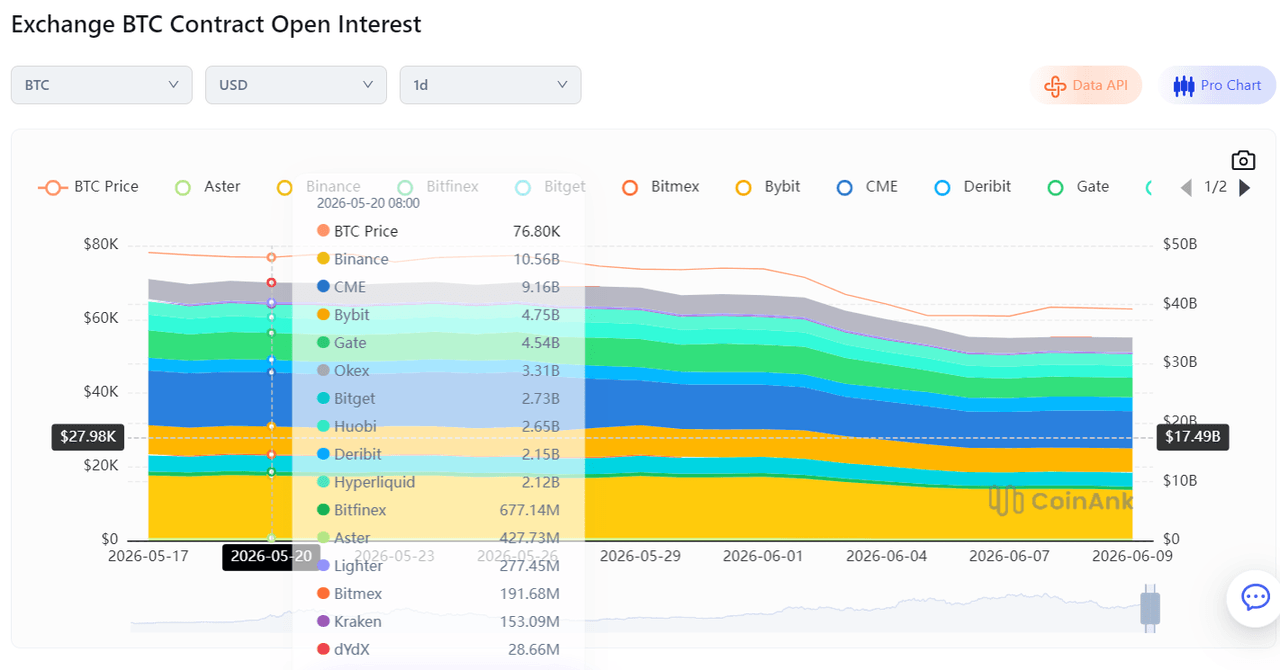

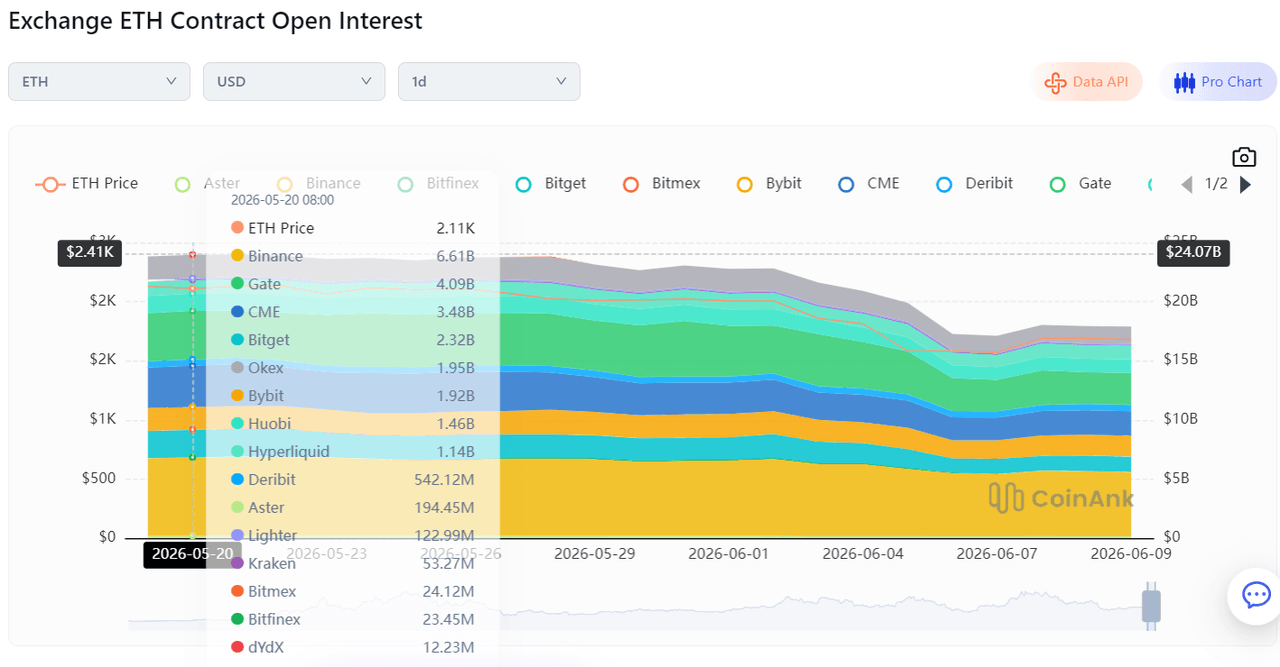

2. Open Interest Changes

Source: https://coinank.com/indexdata/oivol/exOiHist

IV. Global Economic and Crypto Sector Developments

1. Global Macroeconomy

- June 5: The U.S. Central Command reported intercepting Iranian missiles and drones, while Iran claimed another strike on key facilities of the U.S. Fifth Fleet. → Impact: Crypto and U.S. equities, European stocks, gold, and oil all declined, while the U.S. dollar surged.

- June 5: U.S. seasonally adjusted non-farm payrolls for May came in at 172,000. → Result: Negative for gold, silver, and cryptocurrencies (better-than-expected data).

1) May 20: China’s Economic Daily stated that gold has effectively become a risk asset. First, trading is extremely crowded; Second, liquidity shock transmission channels have changed; Third, the pricing logic has fundamentally shifted.

2) May 21: Local police in Albuquerque, New Mexico (U.S.) reported that three family members died after exposure to an unidentified substance, and 18 emergency responders were hospitalized after contact.

3) May 23: Trump reversed his stance, stating that “Warsh will be allowed to decide interest rates,” while U.S. Treasury yields surged, putting pressure on the incoming Fed Chair.

4) May 25: Bank Indonesia raised its benchmark interest rate by 50 bps to 5.25% (market expected a 25 bps hike).

5) May 27: Bank of England Governor Bailey said the central bank may tolerate higher inflation to support the UK economy.

6) May 29: ECB report: Gold has replaced U.S. Treasuries as the world’s preferred reserve asset.

7) May 31: U.S. Central Command: the military redirected 122 commercial vessels away from the Strait of Hormuz to ensure compliance and safety.

8) June 1: Fed Chair Warsh appointed two advisors, both conservatives, to assist with policy analysis and planning.

9) June 3: Renewed conflict in the Gulf region: U.S. forces struck Iran’s Qeshm Island, opened fire on oil tankers, and air defense alerts were activated in Kuwait and Bahrain.

10) June 4: The U.S. House of Representatives passed a resolution limiting Trump’s authority to launch military action against Iran, though it carries no binding legal force.

11) June 6: Bank of Japan Governor Kazuo Ueda stated that further rate hikes are necessary to contain inflation.

12) June 7: CME FedWatch Tool: probability of the Fed keeping rates unchanged in June is 98.4%, while the probability of a 25 bps cut is 1.6%.

13) June 8: The IMF pushed back its projection for the Fed’s return to its 2% inflation target to the end of 2027.

2. Industry Update

- Practical development: Mastercard has partnered with Chainlink to build a direct fiat-to-crypto on-ramp.

- Ecosystem update: Glassnode reports that nearly $500 billion worth of Bitcoin could face potential risk from future quantum computing attacks.

1) May 20: The U.S. Federal Reserve released the 2025 Report on the Economic Wellbeing of U.S. Households, showing that one in four American workers is already using AI at work, while cryptocurrencies are still primarily used for investment purposes.

2) May 22: A custom stablecoin, USDF, has been launched on the Solana blockchain.

3) May 24: Trump Media & Technology Group withdrew its Bitcoin ETF application.

4) May 26: Researchers warned that AI is accelerating the development of quantum computing, posing potential security risks to the crypto industry.

5) May 28: Opinion: HYPE token buybacks could reach several hundred million dollars per quarter, becoming a key driver of price appreciation.

6) May 30: Grayscale expressed strong optimism about Hyperliquid, describing it as a future financial giant and a blueprint for a 24/7 global on-chain financial market.

7) June 1: Yi He was listed in Fortune magazine’s “Most Powerful Women in Business,” becoming the first crypto-native executive to receive the recognition.

8) June 3: Mastercard expanded its on-chain settlement strategy, betting on stablecoins and always-on financial infrastructure.

9) June 4: Curve founder stated that crypto and AI are not competing technologies, but both serve as foundational technologies.

10) June 5: Report: Approximately 70% of global crypto-related violent theft incidents occur in France.

11) June 7: BTC and ETH are on track for their largest weekly decline since the FTX collapse, with $390 billion wiped from the total crypto market capitalization.

12) June 8: Bitcoin experienced a sharp intraday “liquidity sweep,” triggering multiple stop-loss orders, with a whale manually liquidating a $12 million position.

3. Regulatory Policy Update

- Region: May 27 — The U.S. CLARITY Digital Asset Market Clarity Act advanced with bipartisan support, entering a critical legislative stage.

- Focus: May 20 — The EU launched a review of its MiCA regulatory framework, signaling an accelerating global race in crypto regulation.

- Focus: May 20 — China tightened taxation on overseas income, with the CRS 2.0 global tax information exchange system being rolled out at an accelerated pace.

1) May 20: The governor of South Carolina signed a bill establishing a pro-crypto, anti-CBDC legal framework.

2) May 21: The German Bundestag rejected a proposal to increase taxes on cryptocurrencies.

3) May 21: U.S. media reported that the crypto industry has established a “liaison center” in Washington to accelerate regulatory legitimization efforts.

4) May 22: The ECB refused to relax regulation on euro-denominated stablecoins, citing concerns over higher financing costs and interference with interest rate policy.

5) May 22: The U.S. FDIC proposed applying Bank Secrecy Act and sanctions compliance requirements to stablecoin issuers.

6) May 23: The U.S. SEC approved Nasdaq-listed Bitcoin index options.

7) May 23: Australia’s ASIC warned that scammers are targeting retail investors via WhatsApp and fake crypto trading platforms.

8) May 24: The U.S. Congress reintroduced a Bitcoin reserve bill, with Republicans proposing accumulation of up to 5% of global Bitcoin supply.

9) May 25: Russia expanded mining regulations, requiring ASIC mining machines to report network addresses.

10) May 26: The UK imposed sanctions on Huobi and a ruble-backed stablecoin issuer, marking the first bank-level sanctions applied to crypto exchanges.

11) May 27: South Korean police established a task force to combat USDT-related money laundering activities.

12) May 28: Indonesia banned the prediction market platform Polymarket, citing illegal online gambling concerns.

13) May 29: French regulators warned that crypto firms without EU licenses by the end of June may face prosecution.

14) May 30: Texas formed a Strategic Bitcoin Reserve advisory committee, exploring direct custody of Bitcoin.

15) May 31: U.S. Treasury Secretary Bessent said the U.S. has seized approximately $1 billion worth of crypto assets linked to Iran.

16) June 2: The Trump administration imposed sanctions on Nobitex, Iran’s largest crypto exchange, as part of pressure measures against Tehran.

17) June 3: Brazil’s central bank required crypto service providers to undergo financial audits and tightened licensing rules.

18) June 4: The UK FCA warned Premier League clubs that partnerships with unauthorized crypto firms may pose legal and reputational risks.

19) June 5: The U.S. SEC released a draft strategic plan to provide a regulatory foundation for digital assets and clarify jurisdiction with the CFTC.

20) June 6: The UK House of Lords published a 71-page stablecoin report criticizing current regulatory proposals as uncompetitive and urging looser rules.

21) June 7: The U.S. SEC issued a new strategic draft, committing to building a clearer regulatory framework for digital assets.

22) June 8: Russia’s central bank initially allowed retail trading only in Bitcoin, Ethereum, and USDT under new regulatory rules.

V. Market Outlook

The current market is assessed to be in a confirmed bear market. Going forward, it is recommended to shift from a medium-term trading strategy to a long-term positioning approach.

For BTC spot positions, limit sell orders may be placed at $135,900, $122,500, $109,050, and $82,150. Existing positions that are currently underwater can be held patiently until the next bull cycle for breakeven or profit-taking on rallies in stages.

On the downside, accumulation (buy-the-dip) orders for BTC spot may be set at $49,600, $35,450, and $21,300. The previously planned buy order at $15,450 can be removed, as it is considered unlikely that this cycle will revisit the prior bear market bottom.

For ETH spot positions, limit sell orders may be placed at $4,885, $3,485, and $2,200. Accumulation orders may be set at $1,240 and $1,085. Positions should be held patiently for profit realization in the next bull market cycle.

Overall, crypto market bull-bear cycles tend to be shorter compared to traditional equity markets, suggesting faster cycle transitions and more compressed timing for both drawdowns and recoveries.

VI. Risk Alert

1. Macro risks:

The upcoming Fed policy meetings on the 16th and 17th are expected to result in a rate hike. A rate hike by the European Central Bank is also broadly priced in by the market. At the same time, geopolitical tensions between the U.S. and Iran are expected to intensify, increasing systemic macro risk.

2. Industry risks:

During the previous bear market, the collapse of FTX, then the world’s second-largest crypto exchange, accelerated the market downturn. In the current cycle, there remains a risk that a major exchange could also experience a similar failure event.

3. Technical risks:

On May 20, CZ (Changpeng Zhao) stated that if API keys exist in code repositories, they should be immediately reviewed and replaced, even in private repositories, to prevent potential security risks. This warning followed an official GitHub disclosure earlier in the day. GitHub reported that it is investigating unauthorized access targeting internal code repositories. The company stated that there is currently no evidence that customer data stored outside GitHub infrastructure has been affected. However, GitHub continues to monitor its systems for abnormal activity. If any user data or services are confirmed to be impacted, notifications will be issued through established incident response channels.

Trading Advice:

Keep spot positions within ≤75% of total capital, and set dynamic take-profit and stop-loss levels to avoid blindly chasing rallies or selling into weakness with high leverage.

Disclaimer: The data in this report are sourced from publicly available information. FameEX makes no representations on the accuracy or suitability of any official statements made by the exchange regarding the data in this area or any related financial advice.