FameEX Crypto Market Trend | April 21, 2026

2026-04-21 11:59:17

Ceasefire and Hormuz reopening hopes fueled war-end expectations, but Iran’s subsequent closure of the Strait triggered a market pullback and dampened speculative sentiment.

I. Core Market Overview

1. BTC Spot Performance

Price Range: [66,574.2] USD - [78,249.1] USD

Weekly Volatility: [17.54]%

Key Driving Factors:

Primary Factors: The two-week ceasefire between the U.S., Israel, and Iran, along with Iran reopening the Strait of Hormuz, has driven expectations that the war is ending.

Secondary Factor: Iran’s subsequent closure of the Strait of Hormuz triggered a market pullback, along with overall speculative sentiment in the market.

2. Central Bank Policy Updates

Policy Impact Assessment:

Recent remarks from Fed officials have been mixed between hawkish and dovish; a swift resolution of the Iran–Lebanon situation could accelerate the pace of rate cuts.

The European Central Bank is focused on financial stability, and there is a higher likelihood that the ECB will raise rates ahead of the Fed this year and next, which could trigger a round of declines in the cryptocurrency market.

3. Other Key Updates

Dubai’s Virtual Assets Regulatory Authority (VARA) has introduced a new regulatory framework for exchange-traded derivatives (ETDs) offered by crypto trading platforms, clarifying how licensed crypto firms can provide such products in Dubai. The framework is set out in Version 2.1 of VARA’s Rulebook for Trading Platform Services, covering requirements such as client suitability, leverage and margin controls, asset segregation, disclosure standards, and regulatory intervention powers. VARA stated that the framework applies to licensed virtual asset service providers (VASPs) offering trading platform services in Dubai. This update establishes more formal regulatory guardrails for high-risk areas of the crypto market in Dubai and expands oversight beyond spot trading as the emirate broadens its trading rules.

The European Central Bank has formally backed a proposal to centralize supervisory authority over major crypto firms under the European Securities and Markets Authority (ESMA). Under the proposal, oversight of systemically important cross-border entities would shift from national competent authorities to ESMA, covering large crypto-asset service providers (CASPs), trading venues, central counterparties, and central securities depositories. This marks the most significant structural change to the EU’s crypto regulatory framework since the Markets in Crypto-Assets Regulation (MiCA) came fully into force for CASPs at the end of 2024. Under the current MiCA framework, national regulators act as frontline supervisors, while ESMA plays a coordinating role.

On April 16, according to Fortune, top crypto venture capital firms such as Paradigm, Pantera Capital, and a16z have seen their portfolio values shrink amid market downturns and capital distributions to investors. The total assets under management of four crypto funds under a16z Crypto fell by nearly 40% to $9.5 billion between 2024 and 2025, partly due to the firm returning capital to investors in its first three funds. Meanwhile, Multicoin Capital’s assets under management have dropped by more than half, to around $2.7 billion.

II. Market Health Index Analysis (Source: CoinMarketCap)

Source: https://coinmarketcap.com/charts/

Conclusion:

Total market cap continues to rise, with expanding trading volume signaling fresh capital inflows.

The Altcoin Season Index remains in the [25–45] range, indicating capital rotation toward Bitcoin; ETF flows have recorded five consecutive days of net inflows, and the Fear & Greed Index is in neutral-to-greedy territory, reflecting strengthening market confidence.

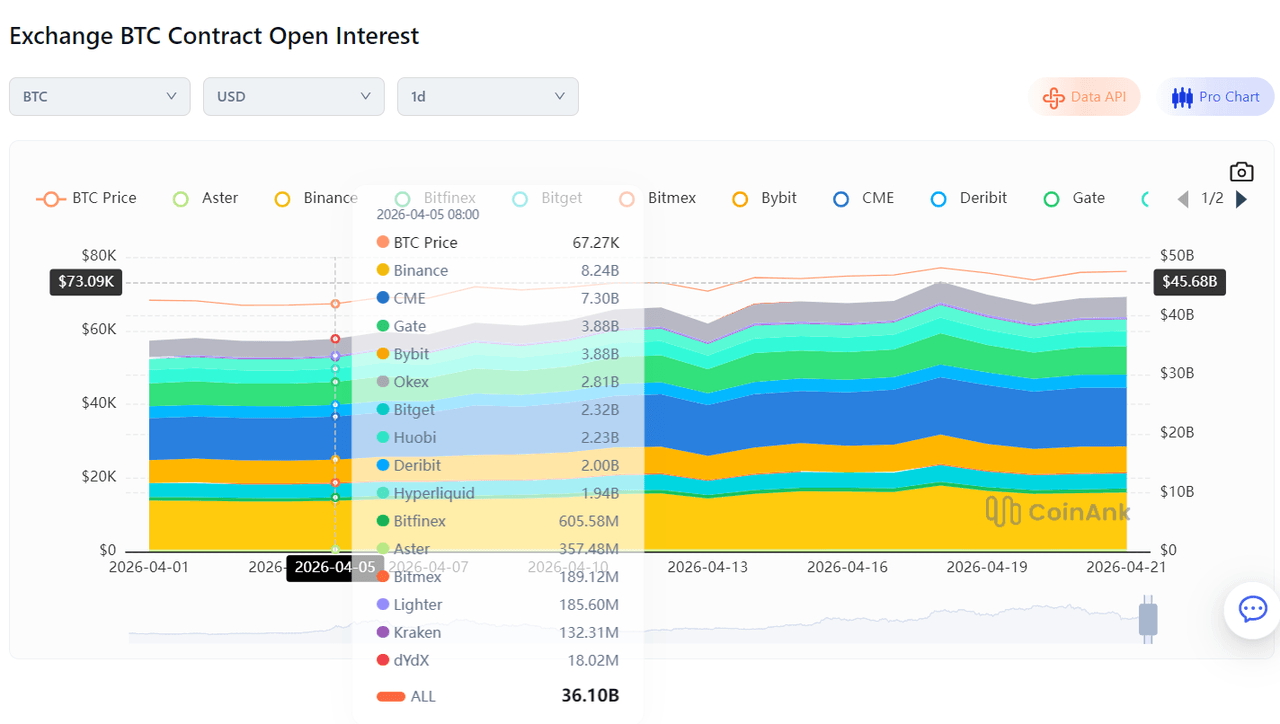

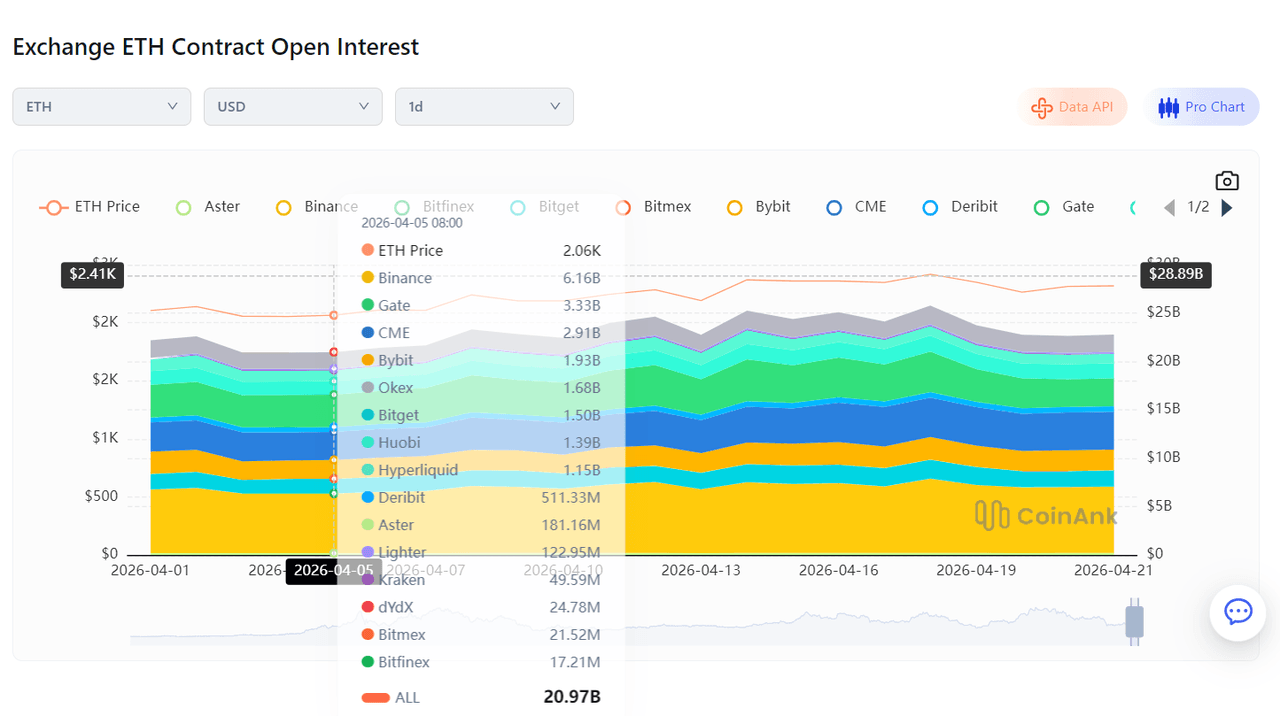

III. Derivatives Monitor (Source: CoinAnk)

1. Funding Rate

30-Day Avg Funding Rate of Bitcoin Across the Top Six CEXs: -0.7168% (Negative)

30-Day Avg Funding Rate of ETH Across the Top Six CEXs: -0.4358% (Negative)

Source: https://coinank.com/fundingRate/current

Interpretation:

Persistently negative funding rates indicate that shorts remain dominant, and overall bearish market expectations have not yet subsided.

2. Open Interest Changes

Source: https://coinank.com/indexdata/oivol/exOiHist

IV. Global Economic and Crypto Sector Developments

1. Global Macroeconomy

- April 18: Iran reopens the Strait of Hormuz [Event] → Impact: Expectations for an end to the current Middle East conflict strengthen [Equities and crypto rise in tandem / Oil prices plunge]

1) April 8: U.S. President Trump agreed to pause bombings and attacks on Iran for two weeks; Pakistan’s Prime Minister stated that the U.S.–Iran ceasefire would take effect at 3:30 a.m. Iran time on April 8.

2) April 8: European Commission Executive Vice President Dombrovskis warned that the ceasefire cannot mask stagflation risks, and growth forecasts may be revised downward.

3) April 9: Trump pressured European allies to submit concrete escort plans within days; Iran’s Revolutionary Guard released safe navigation routes through the Strait of Hormuz to avoid sea mines.

4) April 10: U.S. core PCE inflation (YoY) for February came in at 3.0%, in line with expectations, down from 3.10% previously.

5) April 11: Ukraine’s chief negotiator signaled progress, saying, “We are not far from reaching an agreement.”

6) April 12: The confirmation hearing for Fed Chair nominee Warsh was postponed; the White House is confident he will take over the Fed in May this year.

7) April 13: China’s CPI (YoY) for March was 1.0%, below the 1.20% expectation and down from 1.30% previously.

8) April 14: IMF Managing Director Kristalina Georgieva said the IMF has lowered global growth forecasts due to the Iran conflict.

9) April 15: U.S. assessment: Iran still possesses thousands of ballistic missiles and can deploy launchers from underground facilities.

10) April 16: The U.S. initial jobless claims for the week ending April 11 were 207,000 (vs. 215,000 expected), with the prior figure revised to 218,000; bearish for gold, silver, and crypto.

11) April 16: U.S. media reported that the U.S. is considering unfreezing $20 billion in funds in exchange for Iran halting uranium enrichment.

12) April 17: Gulf and European officials said a U.S.–Iran agreement would take at least six months, not “soon” as Trump suggested; the U.S. military has expanded its blockade of Iranian shipping to include weapons, ammunition, crude oil, refined products, steel, and aluminum.

13) April 18: Iran reopened the Strait of Hormuz.

14) April 18: Bank of England Governor Bailey said there will be no rush to raise rates; Deputy Governor Breeden noted that the Iran conflict increases the likelihood of compounded market stress and could lead to a period of volatility if pressures materialize.

15) April 19: UAE officials reported that in the first 40 days of the conflict, Iran launched over 2,800 attacks, with more than 90% targeting civilian infrastructure.

16) April 19: The U.S. government will begin refunding $166 billion in tariffs imposed during the Trump era.

17) April 20: Iran has agreed to send representatives for a second round of talks this week.

18) April 20: Divisions within the Pentagon have become public, with the U.S. Secretary of Defense and the Army Secretary clashing over personnel disputes.

2. Industry Update

- Ecosystem Update: Vitalik unveils Ethereum’s five-year roadmap.

- Institutional Move: Morgan Stanley’s spot Bitcoin ETF was listed on the NYSE on the evening of April 8.

1) April 8: Morgan Stanley’s spot Bitcoin ETF is set to list on the NYSE tonight, making it the first major U.S. commercial bank to launch a Bitcoin ETF.

2) April 9: CZ (Changpeng Zhao): Quantum computing could potentially break existing cryptocurrency mechanisms.

3) April 10: Chainalysis: Using crypto to pay transit fees through the Strait of Hormuz may face sanctions risks.

4) April 11: Bitcoin mining firms face increasing pressure ahead of the 2028 halving, accelerating a shift toward energy and infrastructure.

5) April 12: Security experts noted that a key difference from other state-backed hackers is that crypto assets have become a direct funding source for military spending.

6) April 13: FBI: Crypto-related fraud losses in the U.S. reached $11.366 billion in 2025, with investment scams as the primary source.

7) April 14: Visa’s Head of Crypto, Cuy Sheffield, said two U.S. banks, Lead Bank and Cross River, have settled transactions using USDC on Solana.

8) April 15: Cato Institute: U.S. Bitcoin tax rules hinder everyday payment use and call for reform.

9) April 15: JPMorgan analysts said negotiations on the U.S. “Crypto Market Structure Bill” (CLARITY Act) have entered the final stage, with both sides working to compromise on remaining issues.

10) April 16: The Ethereum Foundation identified around 100 “state-level hacker infiltrators,” linked to North Korean backgrounds.

11) April 16: Gate Research Institute: Crypto ETFs are increasingly becoming a key liquidity absorption tool in the market.

12) April 17: A wave of shutdowns in the crypto bear market has materialized, with infrastructure and application-layer projects exiting or pivoting.

13) April 17: Crypto fintech firm Superstate launched a new fund operating system, FundOS.

14) April 18: Spark’s Head of Strategy: The ETH market faces liquidity risks due to a potential 10%–15% reduction in rsETH lending.

15) April 18: Galaxy Head of Research: 518 Bitcoin addresses are listed under U.S. OFAC sanctions.

16) April 19: Bank for International Settlements: Globally coordinated stablecoin regulation is crucial to prevent market fragmentation.

17) April 19: Binance Co-CEO He Yi: Blockchain could replace the SWIFT system in the future, with all asset transactions conducted on-chain 24/7.

18) April 20: Vitalik unveiled Ethereum’s five-year roadmap, focusing on post-quantum security, ZK-EVM, and the ultimate resilience of the “world computer.”

19) April 20: HTX DeepThink: The macro logic of the crypto market is shifting from “inflation shock” to “geopolitical easing,” with Bitcoin entering a dual-pricing phase driven by liquidity and risk appetite.

3. Regulatory Policy Update

- Region: UK FCA releases final draft of crypto asset framework [Europe] → [Bill Passed]

- Focus: The White House approves review of a proposal to include cryptocurrencies in 401(k) retirement plans [Tax Policy]

1) April 5: China’s State Taxation Administration encouraged banks and tax authorities to leverage blockchain and privacy computing to innovate the “bank–tax interaction” model.

2) April 6: New South Korean regulations require crypto exchanges to verify asset holdings every five minutes; the central banks of France and South Korea launched cooperation on tokenized cross-border payments and digital asset frameworks.

3) April 7: South Korea required crypto exchanges to standardize withdrawal delay rules to combat voice phishing scams.

4) April 8: The U.S. SEC withdrew multiple crypto enforcement actions, shifting focus to substantive fraud cases.

5) April 9: The U.S. FDIC issued stablecoin guidelines covering reserve assets and capital requirements.

6) April 10: The Hong Kong Monetary Authority announced the first batch of stablecoin licenses, granted to RD Innotech (a joint venture of Standard Chartered Hong Kong, HKT, and Animoca Group) and HSBC.

7) April 11: The People’s Bank of China added 12 new digital yuan operating institutions.

8) April 12: Argentina included cryptocurrencies in the net worth criteria for qualified investors.

9) April 13: The Bank of Korea proposed introducing circuit breakers in the crypto market following the Bithumb operational incident.

10) April 14: Cambodia’s National Assembly unanimously passed a new anti-cyber fraud law targeting large-scale scam operations using crypto assets, with penalties up to life imprisonment.

11) April 15: The U.S. CFTC Chair stated that oversight of prediction markets falls exclusively under federal jurisdiction, with no authority for states to intervene.

12) April 16: The UK FCA released the final draft of its crypto asset framework, bringing activities such as token custody beyond 24 hours and automated permissions under regulation.

13) April 17: A French minister announced new measures to address the rise in crypto-related kidnapping cases.

14) April 18: South Korea piloted blockchain-based deposit tokens for government spending.

15) April 19: Public consultation on China’s Financial Law draft concluded, with limited coverage of the legal status of digital currencies and crypto asset regulation boundaries.

16) April 20: Hong Kong’s Securities and Futures Commission released a regulatory framework for secondary market trading of tokenized investment products.

V. Market Outlook

From April 22 to May 30, the medium-term trading strategy will still be applied: for the BTC spot, maintain the sell order at $135,900, positioning for the view that the current crypto bull cycle is not yet over, followed by a major rebound. Place the buy orders at $52,800, $21,300, and $15,450, respectively.

For the ETH spot, place sell orders at $3,485 and $4,885. Set dip-buying spot orders at $1,240 (keep active) and $815.

Recent economic data has had a limited impact on crypto market volatility, while the Middle East conflict continues to dominate investor sentiment across asset classes. A peace agreement between the U.S., Israel, and Iran remains possible, but so does further escalation. In this environment, it may be prudent to avoid frequent trading to reduce the risk of being whipsawed by rapid shifts between long and short positions. Looking ahead, the Federal Reserve’s rate decision at the end of this month will be a key event. Market consensus expects rates to remain unchanged, with attention focused on the potential for rate cuts. A rate cut would exceed expectations and could trigger a modest rally in the crypto market; conversely, a rate hike would likely provoke a stronger reaction, with a high probability of a notable downturn in crypto prices.

On April 17, crypto market analyst Axel reported that since early 2026, capital has continued to flow out of the Bitcoin network, leading to a persistent decline in realized market capitalization, with growth rates remaining negative. The 30-day change in realized cap currently stands at -0.32%, an improvement from -0.54% in early April, indicating that outflows are slowing, but a reversal has yet to be confirmed. Axel noted that as long as the growth differential remains negative, the market is still in a structurally defensive bear phase, and a bullish reversal would require renewed capital inflows.

On April 20, Bitmine Chairman Thomas “Tom” Lee stated that there are increasing signs the “mini crypto winter” is nearing its end. As downside risks from the U.S.–Iran conflict recede, ETH has rebounded 41% from its early February lows. Since the outbreak of the conflict, ETH has outperformed the S&P 500 by 2,280 basis points and remains one of the best-performing global assets (excluding oil). Ethereum continues to benefit from two major narratives: the tokenization of assets by Wall Street and the growing demand from agent-based AI systems for neutral, public blockchains. In this view, ETH’s role as a “wartime store of value” and its market leadership since the conflict began are significant. While some expect the crypto winter to last until autumn 2026, Lee maintains that it is already nearing its end. Since 2015, major crypto winters have coincided with equity market corrections of at least 20%. In contrast, the 2026 equity pullback has been relatively mild at around -8%, compared to the roughly 20% decline seen alongside the 2025 crypto downturn.

VI. Risk Alert

1. Macro Risks: Failure of the second round of U.S.–Iran talks; the U.S. could deploy ground forces to seize control of the Strait of Hormuz and send special forces into Iran to capture or destroy enriched uranium. NATO members, along with Japan and South Korea, may dispatch naval forces to assist in maintaining a maritime blockade of Iran. Continued Israel–Lebanon fighting with little prospect of near-term reconciliation could further escalate tensions in the Middle East. [Geopolitical escalation, etc.]

2. Industry Risks: Potential leakage of exchange user data

3. Technical Risks: None at present. [Abnormal whale address activity / Sharp spikes in on-chain gas fees, etc.]

Trading Advice:

Keep spot positions within ≤85% of total capital, and set dynamic take-profit and stop-loss levels to avoid blindly chasing rallies or selling into weakness with high leverage.

On March 28, cybersecurity platform VECERT disclosed that a hacker operating under the alias “PexRat” was selling a database on the dark web containing personal information of 1.5 million Binance users. The data reportedly includes names, email addresses, phone numbers, KYC verification status, login IP addresses, and two-factor authentication methods. Analysis suggests the incident did not involve a direct breach of Binance’s internal servers. Instead, the attacker bypassed CAPTCHA protections and obtained the data through credential stuffing and automated scraping. Affected users face heightened risks of SIM-swapping and phishing attacks. The incident comes as Binance’s institutional OTC trading business is experiencing rapid growth, with trading volume in January–February alone reaching 25% of the total for all of 2025. This marks another data security challenge for Binance, following the leak of 420,000 sets of account credentials in January.

Disclaimer: The data in this report are sourced from publicly available information. FameEX makes no representations on the accuracy or suitability of any official statements made by the exchange regarding the data in this area or any related financial advice.