FameEX Crypto Market Trend | March 3, 2026

2026-03-03 15:45:40

I. Core Market Overview

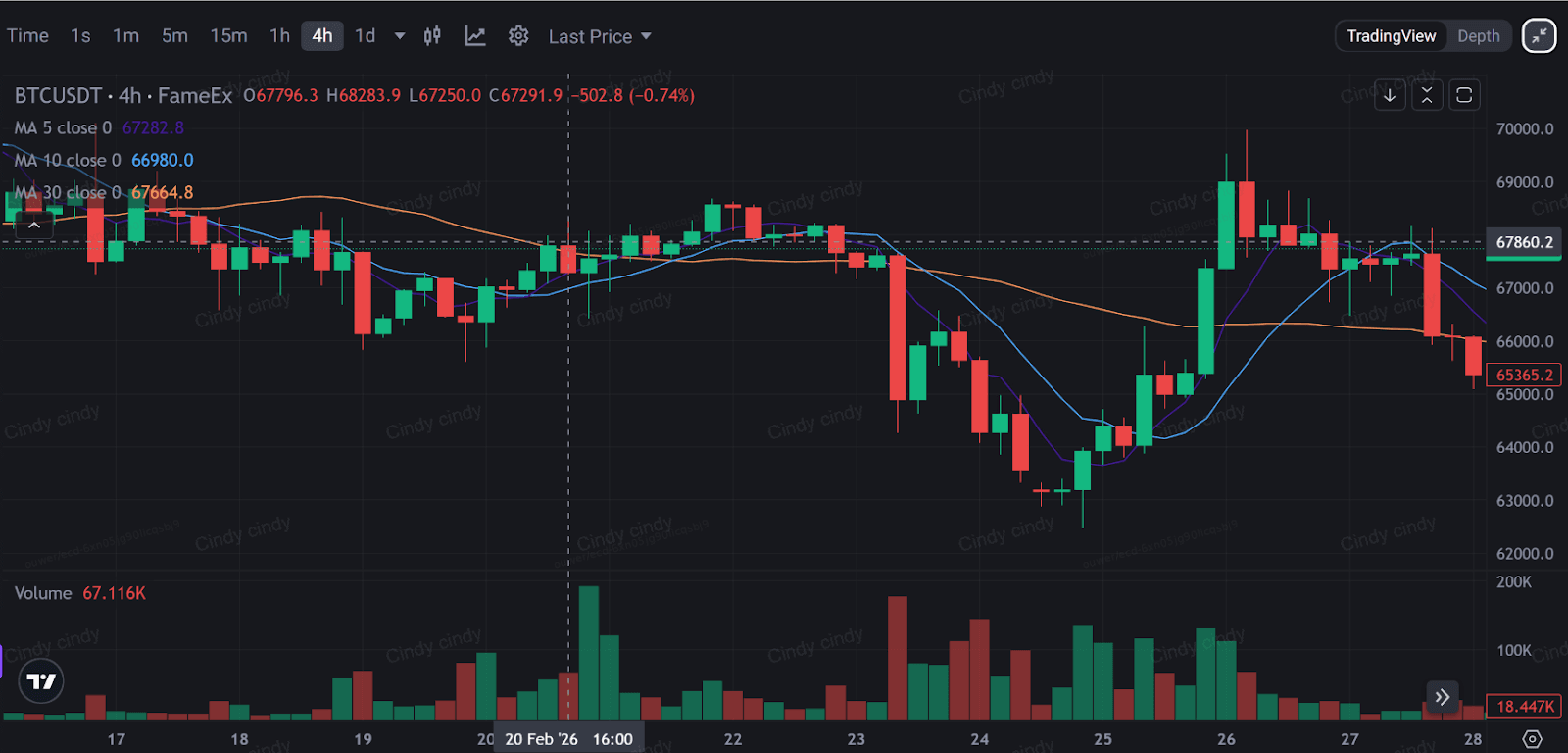

1. BTC Spot Performance

Price Range: [ 62,464.2 ] USD - [ 70,104.1 ] USD

Weekly Volatility: [12.23]%

Key Driving Factors:

Primary Factors: Yen rate hikes / Potential U.S. dollar tightening / Concerns over a U.S.–Iran conflict / Federal Reserve leadership succession, including Trump’s nomination of hawkish candidate Warsh, etc.

Secondary Factor: Most retail investors believe the crypto bear market has already begun.

2. Central Bank Policy Updates

Policy Impact Assessment:

The Fed is leaning [dovish], signaling a potential shift toward [rate cut expectations], with multiple Fed officials expressing dovish views. The secondary scenario is to keep rates unchanged.

The ECB is currently focused on [financial stability], with crypto asset regulation trending [more accommodative].

3. Other Key Updates

A report titled “Ready Player One”: An In-Depth Analysis of the Global Virtual Currency Asset Harvesting Under the U.S. Technological Hegemony”, jointly released by the China National Computer Virus Emergency Response Center and other institutions, outlines what it describes as the United States’ use of technological dominance to seize global virtual currency assets. According to incomplete statistics cited in the report, from 2022 to 2025 the U.S. confiscated more than $30 billion worth of global virtual currency assets through various cases. In the Chen Zhi case alone, seized assets reportedly totaled $15 billion, accounting for approximately 50% of the total.

The report further claims that between 2023 and 2025, hacker groups allegedly backed by the U.S. government launched targeted attacks on more than 20 major global virtual asset exchanges. Attack methods included backdoor implantation, spear phishing, and supply chain infiltration. The primary objectives were to steal users’ wallet private keys, platform transaction records, and regulatory compliance data. Targeted platforms spanned multiple countries and regions across Asia, Europe, and Africa.

A latest report from Crypto.com indicates that the number of global cryptocurrency holders rose from 659 million in 2024 to 741 million in 2025, representing a 12.4% year-on-year increase. The growth was primarily driven by rising institutional adoption and pro-crypto policies in the United States, including the establishment of a Bitcoin strategic reserve. In terms of holder composition, Bitcoin holders increased by 8.3% to 365 million, accounting for nearly half of the global total. Ethereum holders grew by 22.6% to 175 million, representing approximately 24%.

Uniswap founder Hayden Adams has warned that fraudulent search engine advertisements impersonating Uniswap continue to appear, with some users losing their entire high-value crypto holdings as a result. Scammers purchase keywords such as “Uniswap” to place fake websites at the top of search results. These websites closely resemble the official platform. Once users connect their wallets and authorize transactions, funds can be immediately drained.

II. Market Health Index Analysis (Source: CoinMarketCap)

Source: https://coinmarketcap.com/charts/

Conclusion:

Total market capitalization is consolidating with a pullback, while the 24-hour trading volume has expanded, suggesting fresh capital entering the market for positioning.

The Altcoin Season Index remains within the 25–95 range, indicating capital concentration toward Bitcoin. Meanwhile, ETF flows have recorded approximately five consecutive days of net inflows. Combined with the Fear & Greed Index rebounding into the “Fear” zone, this suggests market confidence is gradually strengthening.

III. Derivatives Monitor (Source: CoinAnk)

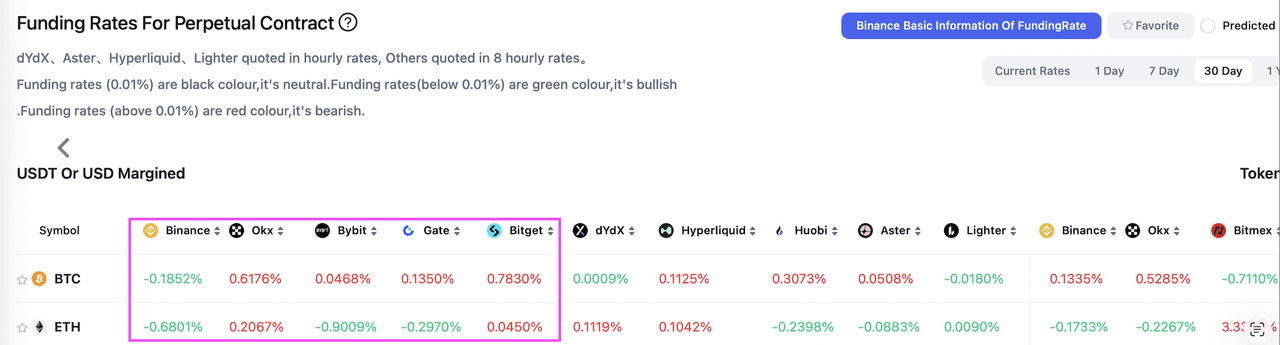

1. Funding Rate

30-Day Avg Funding Rate of Bitcoin Across the Top Five CEXs: 0.2786% (Positive)

30-Day Avg Funding Rate of ETH Across the Top Five CEXs: -0.3326% (Negative)

Source: https://coinank.com/fundingRate/current

Interpretation:

1) The average BTC funding rate across the top five crypto exchanges remains positive, though Binance continues to dominate the market with an overwhelming share.

2) The average ETH funding rate is negative, indicating that short positions currently dominate the broader market, reinforcing bearish expectations.

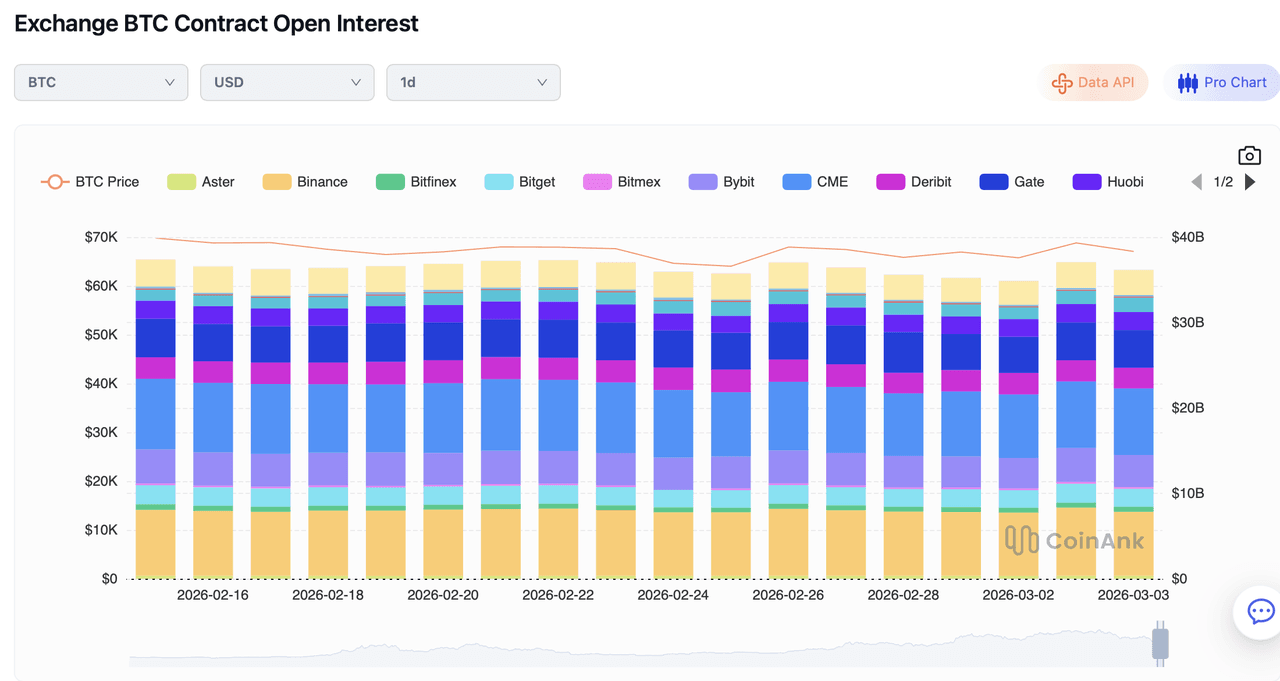

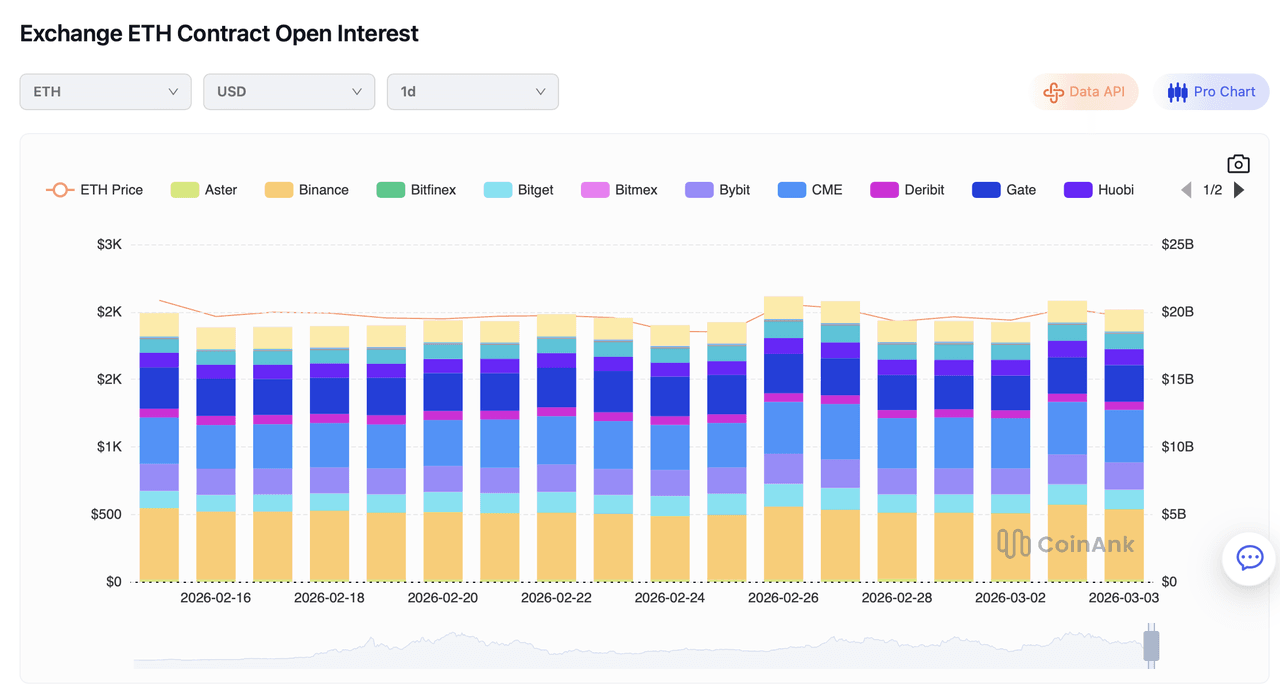

2. Open Interest Changes

Source: https://coinank.com/indexdata/oivol/exOiHist

IV. Global Economic and Crypto Sector Developments

1. Global Macroeconomy

- Feb 28: [The U.S. and Israel killed Iran’s supreme leader; Iran closed the Strait of Hormuz] → Impact: [Global equities declined in tandem / Gold and oil prices surged]

- Feb 26: [U.S. weekly initial jobless claims released] → Result: [Came in below expectations]

1) Feb 16 – U.S. Treasury Secretary Scott Bessent said inflation may ease toward 2% by mid-2026 and reiterated that 2025 GDP growth could reach 3%. The Senate Banking Committee advanced Warsh’s Fed nomination.

2) Feb 17 – Bank of England Chief Economist Huw Pill stated monetary policy remains restrictive, with underlying inflation expected to reach 2.5%. UK January CPI MoM: -0.5%, the largest decline since January 2024.

3) Feb 23 – Bank of England MPC member Alan Taylor said rates are approaching neutral but have not yet reached it; two to three additional rate cuts may be required before neutrality.

4) Feb 24 – A White House official said President Trump’s proposed 15% tariff plan under Section 122 remains unchanged, though the timing is unclear. A new 10% import tariff has officially taken effect.

5) Feb 25 – Eurozone January CPI final MoM: -0.6% (vs. -0.5% expected, prior -0.5%). Eurozone January CPI final YoY: 1.7% (in line with expectations and prior).

6) Feb 25 – Bank of England Governor Andrew Bailey said further policy easing is likely this year; the March rate decision is finely balanced. Chief Economist Pill added that disinflation continues but is not yet complete, and core inflation must be monitored closely.

7) Feb 26 – The Trump administration considered requiring banks to collect customers’ citizenship information as part of immigration enforcement efforts.

8) Feb 26 – U.S. weekly initial jobless claims (week ending Feb 21): 212,000 vs. 215,000 expected; prior revised to 208,000 from 206,000. Bearish for gold, silver, and crypto.

9) Feb 26 – U.S. weekly initial jobless claims (week ending Feb 21): 212,000 vs. 215,000 expected; prior revised to 208,000 from 206,000.

10) Feb 27 – U.S. January PPI MoM: 0.5% vs. 0.3% expected; prior revised to 0.4% from 0.5%.

11) Mar 1 – Bank of Japan Deputy Governor Ryozo Himino said policy remains somewhat accommodative but should gradually move toward neutrality through moderate rate hikes.

12) Mar 1 – Armed clashes erupted again along the Pakistan–Afghanistan border, according to Afghan border police.

13) Mar 2 (morning, local time) – Air raid sirens sounded in Manama, Bahrain, with explosions reported. Explosions were also reported in Doha and Dubai. Iran’s military stated it launched additional missiles toward Israel.

14) Mar 2 – Trump claimed 48 Iranian leaders, including Khamenei, were killed in coordinated strikes, allegedly destroying Iran’s naval headquarters. U.S. forces stated they destroyed the IRGC headquarters and would continue bombing operations for up to four weeks until objectives are achieved. Sanctions could be lifted if Iran’s next leadership adopts a pragmatic stance.

15) Mar 2 – Iran established an interim leadership council including President Pezeshkian, the justice minister, and jurist Alireza Arafi. Security Council Secretary Larijani said Iran will not negotiate with the U.S.

16) Mar 2 – ABC News reported that the U.S. House of Representatives is expected to vote on a War Powers Resolution requiring congressional approval before further military action.

17) Mar 2 – France, the UK, and Germany issued a joint statement indicating that defensive measures could include eliminating Iran’s missile and drone launch capabilities. Iran warned that if its energy facilities are attacked, all oil and gas infrastructure across the Middle East would be destroyed.

18) Mar 2 – Escalation in the Middle East triggered a global risk-off wave: gold, silver, and oil surged, while U.S. stock futures declined.

2. Industry Update

1) Feb 16 – U.S. Treasury Secretary Scott Bessent (on crypto) said it is crucial to finalize the legislation as soon as possible, and President Trump is expected to sign it this spring.

2) Feb 18 – Emirates NBD enabled the possibility of allocating Bitcoin within its investment process.

3) Feb 19 – Moody’s warned that the AI race poses significant financial risks, with $662 billion in obligations not yet reflected on major tech companies’ balance sheets.

4) Feb 21 – Binance Research stated that market concerns about AI disrupting the software sector may be overstated, and Bitcoin is nearing a structural bottom.

5) Feb 22 – JPMorgan said that if the U.S. Crypto Market Structure Bill is passed before July 1 this year, it would provide a boost to the market.

6) Feb 23 – Morgan Stanley, which manages nearly $9 trillion in assets, planned to launch Bitcoin custody, trading, yield, and lending services.

7) Feb 24 – Ethereum proposed a roadmap to address quantum computing threats and released a “strawman roadmap,” aiming to mitigate future quantum risks through new signature and data schemes, while targeting second-level transaction speeds and significantly higher throughput.

8) Feb 25 – Citibank planned to launch institutional-grade Bitcoin custody services this year.

9) Feb 26 – UK banking giant Barclays explored a blockchain-based payments platform that could incorporate stablecoins and tokenized deposits.

10) Feb 27 – Gate Research reported that gold and silver prices have reached record highs, driving significant expansion in the tokenized commodities sector.

11) Feb 28 – TRM Labs reported that AI-driven crypto scams surged 500% year-on-year in 2025.

12) Mar 1 – The Central Bank of Russia warned that financial pyramid scheme organizers in the country have increasingly shifted to using cryptocurrencies.

13) Mar 1 – Arthur Hayes stated that prolonged U.S. involvement in the Iran conflict would force the Fed to print money, pushing Bitcoin prices higher.

14) Mar 2 – As U.S.–Iran tensions escalated and traditional financial markets were closed over the weekend, crypto derivatives platform Hyperliquid became a key venue for investors hedging commodity risks.

15) Mar 2 – Mastercard was recruiting a Head of Crypto Liquidity as part of its expansion into the DeFi space.

3. Regulatory Policy Update

· Region: The U.S. Crypto Market Structure Bill has entered the refinement and review stage; U.S. lawmakers have introduced the Blockchain Innovation and Development Promotion Act of 2026.

- [U.S. / EU] → [Legislative Review Stage]

- Focus: UK regulators plan to allow cryptocurrencies for gambling payments. [Crypto Adoption]

1) Feb 18 – The People’s Bank of China and seven other ministries stated they will continue cracking down on virtual currency mining activities.

2) Feb 19 – Elliptic reported that five crypto exchanges have helped Russia circumvent U.S. sanctions, filling the gap left after Garantex was shut down.

3) Feb 19 – Missouri’s Bitcoin Strategic Reserve Bill entered review in the State House Commerce Committee.

4) Feb 20 – Russia launched a criminal investigation into Telegram founder Pavel Durov over alleged assistance in terrorist activities.

5) Feb 20 – The Fed considered permanently removing “reputational risk” from supervisory criteria, potentially easing debanking pressures on crypto firms.

6) Feb 22 – South Africa planned to revise regulations to incorporate crypto assets into its capital flow management framework.

7) Feb 23 – South Korea proposed legislation requiring crypto KOLs to disclose holdings and compensation, with violations potentially treated as market manipulation.

8) Feb 24 – President Trump called for the immediate passage of the Ban on Insider Trading Act to prevent members of Congress from profiting from non-public information.

9) Feb 25 – President Putin signed a law granting Russian courts authority to confiscate cryptocurrencies such as Bitcoin in criminal investigations.

10) Feb 25 – A legal applicability hearing in the 60,000 BTC money laundering case involving Qian Zhimin was scheduled for July at the UK High Court. The claims registration deadline was set for May 22, with more than 11,300 Chinese victims having filed applications.

11) Feb 27 – China’s Supreme People’s Court stated that future enforcement will focus on crimes linked to virtual currencies and underground banking, including money laundering.

12) Feb 27 – Indiana’s Bitcoin Rights Bill passed both chambers of the state legislature and awaited final signature.

13) Feb 28 – The Netherlands planned to amend a controversial bill taxing unrealized crypto gains.

14) Feb 28 – UK regulators considered allowing cryptocurrencies for gambling payments. Starting next fiscal year, crypto ETNs will be banned from mainstream ISA tax-free accounts.

15) Mar 1 – Minnesota introduced a bill to ban the placement and operation of crypto ATMs to combat scams targeting the elderly.

16) Mar 2 – U.S. lawmakers introduced the Blockchain Innovation and Development Promotion Act of 2026, aimed at reducing the risk of improper criminal charges against developers.

V. Market Outlook

From March 4 to March 31, the medium-term trading strategy will still be applied: for the BTC spot, maintain the sell order at $135,900, positioning for the view that the current crypto bull cycle is not yet over, followed by a major rebound. Place the buy orders at $52,800, $21,300, and $15,450, respectively.

For the ETH spot, place sell orders at $3,485 and $4,885. Set dip-buying spot orders at $1,240 (keep active) and $815.

VI. Risk Alert

1) Macro Risks: [Fed policy shift / Escalation of geopolitical conflicts, etc.]

If the U.S. were to become entangled in a prolonged conflict similar to the Iraq War, it would likely have a medium- to long-term (over one year) bearish impact on the crypto industry. That said, both the U.S. military and government are expected to make significant efforts to avoid repeating past mistakes in handling the Iran situation.

2. Industry Risks: None at present. [Exchange collapses / Sudden regulatory crackdowns, etc.]

3. Technical Risks: None at present. [Abnormal whale address activity / Sharp spikes in on-chain gas fees, etc.]

Trading Advice:

After the release of the minutes from the current round of the Fed’s March 19 policy meeting, the cryptocurrency market is expected to end its narrow-range consolidation. Keep spot positions within ≤90% of total capital, and set dynamic take-profit and stop-loss levels to avoid blindly chasing rallies or selling into weakness with high leverage.

On Feb 27, Swyftx Chief Analyst Pav Hundal stated that Ethereum has already priced in a significant amount of short-term uncertainty and may remain subdued in the coming weeks. “A large amount of short-term uncertainty has been priced into Ethereum. I wouldn’t be surprised if ETH remains relatively sluggish over the next few weeks,” Hundal added. He noted that geopolitical tensions, including the escalation of the Iran situation, as well as progress on the U.S. Crypto Clarity Act, have largely been absorbed by the market. The $19 billion liquidation event last October continues to weigh on the market.

Since February this year, BTC has recorded its fifth consecutive monthly decline, marking the first similar streak since the end of the 2018 bear market. Historical data show that after five consecutive monthly losses in 2018–2019, BTC subsequently posted five straight monthly gains, rallying more than 300%. If the cycle repeats, a potential reversal window could point to April this year.

Disclaimer: The data in this report are sourced from publicly available information. FameEX makes no representations on the accuracy or suitability of any official statements made by the exchange regarding the data in this area or any related financial advice.