FameEX Crypto Market Trend | March 26, 2026

2026-03-26 06:27:24

I. Core Market Overview

1. BTC Spot Performance

Price Range: [ 67,276.8 ] USD - [ 75,040.3 ] USD

Weekly Volatility: [11.54]%

Key Driving Factors:

Primary Factors:

1) The U.S. and Israel struck Iran, which continues missile and drone attacks on neighboring countries.

2) The Fed’s March meeting saw no major changes, in line with expectations.

3) Other major economies (EU, UK, China, Japan, Canada) also kept rates unchanged this month.

Secondary Factor: [Market sentiment]

2. Central Bank Policy Updates

Policy Impact Assessment:

The Fed is leaning dovish, signaling a potential shift toward rate cut expectations.

The ECB’s primary focus remains on combating inflation, with financial stability as a secondary priority; the stance on the strictness of crypto asset regulation remains unchanged.

3. Other Key Updates

Key Takeaways from the Federal Reserve’s March FOMC Statement and Powell’s Press Conference

[FOMC Statement]

1) Rate Decision: The policy rate was kept unchanged at 3.5%–3.75%, marking the second consecutive pause; Governor Milan dissented, favoring a 25 basis point rate cut.

2) Rate Outlook: The median dot plot continues to project one rate cut in 2026 and one in 2027; the median estimate for the longer-run federal funds rate was revised slightly higher.

3) Inflation Outlook: Inflation remains somewhat elevated. The Fed remains firmly committed to returning inflation to its 2% target. PCE and core PCE inflation forecasts for the next two years were revised upward.

4) Economic Outlook: Uncertainty around the economic outlook remains elevated. The impact of developments in the Middle East on the U.S. economy is still unclear. Growth forecasts for the next three years were revised upward.

5) Labor Market: Job growth has remained subdued in recent months, while the unemployment rate has been broadly stable. The unemployment rate forecast for this year was unchanged, while next year’s forecast was raised to 4.3%.

[Powell Press Conference]

1) Rate Outlook: The Fed is in a favorable position. The policy rate is at the upper end of the neutral range, or slightly restrictive. If inflation does not improve, rate cuts will not occur. While most do not view rate hikes as the baseline, the possibility of a hike as the next move has been discussed. No specific triggers for a rate hike were identified.

2) Inflation Outlook: Rising energy prices will push up headline inflation, though it is too early to assess the magnitude. The current energy supply shock is viewed as a one-off event. Whether energy-driven inflation can be looked through depends on containing goods inflation. Slow progress on tariffs is affecting inflation forecasts.

3) Economic Outlook: The U.S. economy remains resilient amid multiple challenges. Higher GDP projections reflect confidence in productivity. Current productivity gains are not driven by generative AI. It is too early to assess the full economic impact of the Middle East situation.

4) Labor Market Outlook: The breakeven level for job creation is clearly low. Multiple indicators suggest some degree of stability in the labor market, though downside risks remain.

5) Tenure Issue: If a new Fed Chair is not confirmed by the end of the term, Powell would serve as acting Chair. There is no intention to leave the Board before the Department of Justice investigation concludes, and future plans remain uncertain thereafter.

6) Market Reaction: From the announcement to the end of Powell’s remarks, gold fell by $30; the Nasdaq’s decline widened from 0.5% to over 1%; the 2-year U.S. Treasury yield rose by about 4 bps; the U.S. dollar gained around 20 points; rate futures reduced pricing for total rate cuts this year by about 3.5 bps, to 17 bps.

II. Market Health Index Analysis (Source: CoinMarketCap)

Source: https://coinmarketcap.com/charts/

Conclusion:

Total market capitalization continues to rise, while declining trading volume suggests a market driven by existing liquidity (a zero-sum dynamic).

The Altcoin Season Index is in the [35–100] range, indicating capital rotation toward mid- and small-cap tokens. ETF flows have recorded consecutive weeks of net outflows; combined with the Fear & Greed Index remaining in the fear zone, this reflects a divergence in market confidence.

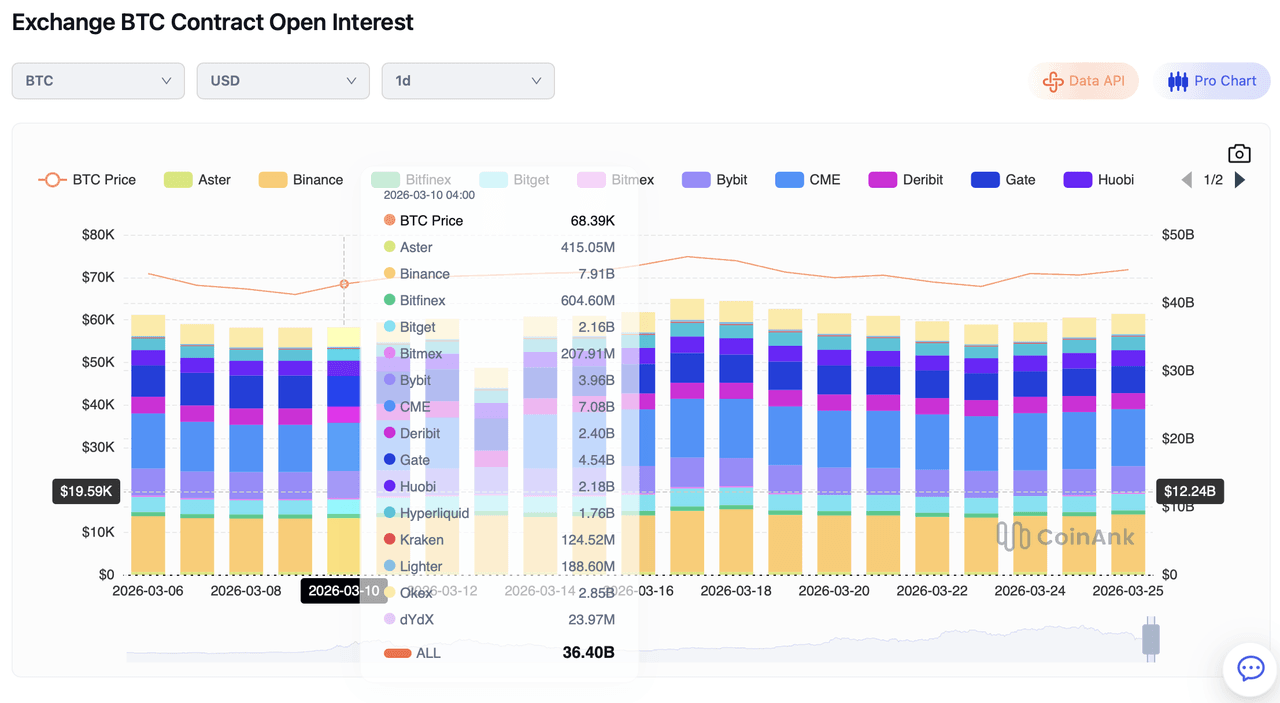

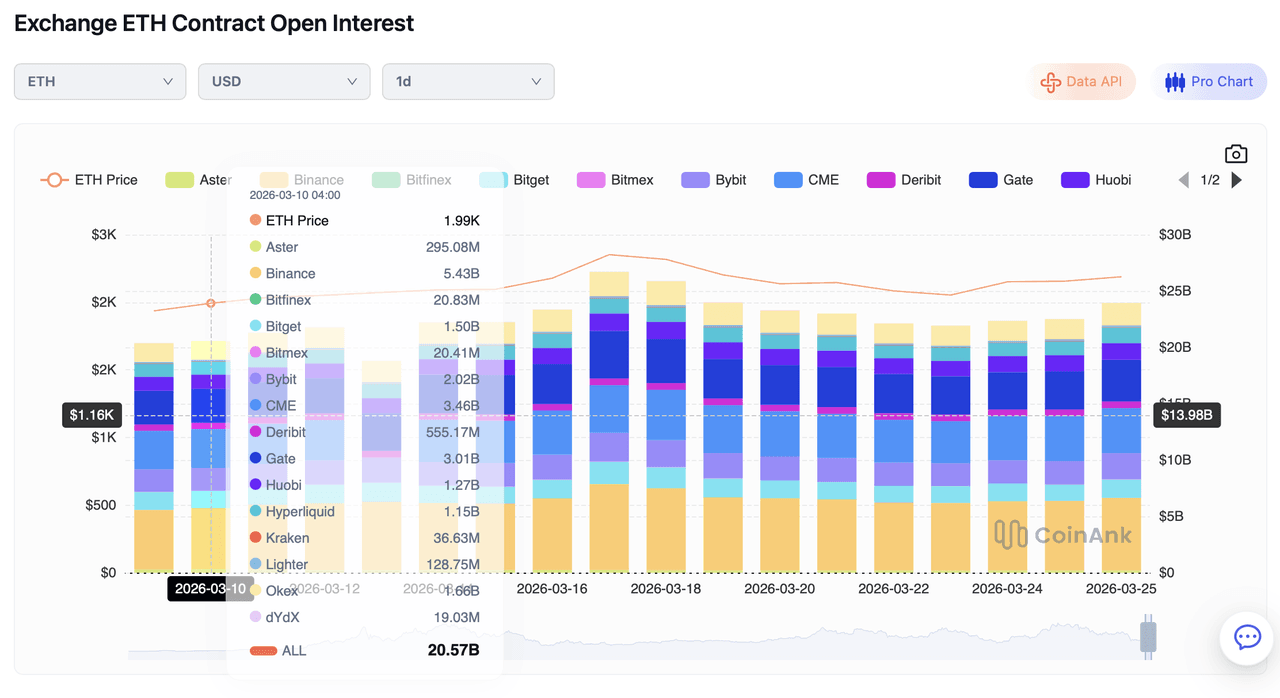

III. Derivatives Monitor (Source: CoinAnk)

1. Funding Rate

30-Day Avg Funding Rate of Bitcoin Across the Top Six CEXs: -0.2026% (Negative)

30-Day Avg Funding Rate of ETH Across the Top Six CEXs: -0.6906% (Negative)

Source: https://coinank.com/fundingRate/current

Interpretation:

Persistently negative funding rates indicate that short positions dominate the market, reinforcing bearish expectations.

2. Open Interest Changes

Source: https://coinank.com/indexdata/oivol/exOiHist

IV. Global Economic and Crypto Sector Developments

1. Global Macroeconomy

- March 13: [Iran’s new Supreme Leader delivers first speech] → Impact: [Global equities and cryptocurrencies move in tandem / U.S. Dollar Index volatility]

- March 19: [The Federal Reserve keeps rates unchanged at 3.5%–3.75%] → Outcome: [In line with market expectations]

1) March 11: U.S. February unadjusted core CPI YoY came in at 2.5% (expected 2.5%, previous 2.50%); February seasonally adjusted CPI MoM was 0.3% (expected 0.3%, previous 0.20%) — both in line with market expectations.

2) March 12: The U.S. launched Section 301 investigations into 16 trading partners, including the EU, aiming to reimpose tariff pressure; a European Commission spokesperson stated the EU would respond firmly and proportionately to any U.S. violations of agreements.

3) March 13: The People’s Bank of China stated it will continue implementing a moderately accommodative monetary policy and strengthen counter-cyclical and cross-cyclical adjustments.

4) March 13: Iran’s new Supreme Leader delivered his first speech: the Strait of Hormuz will remain closed; U.S. military bases will be targeted if they do not withdraw; if the war continues, additional fronts will be opened.

5) March 14: According to three U.S. officials, about 5,000 U.S. Marines and sailors are being deployed to the Middle East to support operations related to Iran; Trump said the economy would rebound immediately once the Iran war ends.

6) March 14: The nomination of Warsh as Fed Chair was blocked, with Republican senators calling for the investigation into Powell to be completed first; a U.S. federal judge revoked DOJ subpoenas issued to the Federal Reserve and Powell.

7) March 17: Bank of Japan Governor Kazuo Ueda stated that appropriate policy decisions will be made to achieve price stability; if yields rise sharply, the BOJ will conduct flexible bond-buying operations.

8) March 18: The U.S. February PPI YoY recorded 3.4% (expected 2.9%), the highest since February last year; the February PPI MoM was 0.7% (expected 0.3%, previous 0.50%) — bearish for gold, silver, and cryptocurrencies.

9) March 18: Eurozone February final CPI MoM came in at 0.6% (expected 0.70%, previous 0.70%) — bearish for gold, silver, and cryptocurrencies.

10) March 19: The ECB kept the deposit facility rate, main refinancing rate, and marginal lending rate unchanged at 2%, 2.15%, and 2.40%, respectively — in line with expectations, marking the sixth consecutive meeting without changes.

11) March 19: The U.S. initial jobless claims for the week ending March 14 came in at 205,000, the lowest since the week of January 10 (expected 215,000) — bearish for gold, silver, and cryptocurrencies.

12) March 20: ECB sources indicated that a rate hike in April is unlikely, with June more probable; however, unless the Middle East conflict is resolved quickly, discussions on rate hikes may need to begin in April, as baseline forecasts are seen as outdated.

13) March 22: PBOC Governor Pan Gongsheng stated that a moderately accommodative monetary policy will continue.

14) March 23: Trump said broader negotiations with Iran are underway; Iran seeks peace and has agreed not to possess nuclear weapons; a five-day deadline has been given; the Strait of Hormuz could be jointly controlled by both sides; once an agreement is reached, oil prices would drop sharply.

15) March 24: Sources said Saudi Arabia has informed the U.S. it is prepared to take military action if Iran attacks its power and water facilities; Israeli media reported Saudi Arabia and the UAE are “gradually” considering joining actions against Iran; Iran and the U.S. are set to hold talks in Pakistan this week; the U.S. has set April 9 as a target date to end the war.

16) March 24: Eurozone March flash manufacturing PMI came in at 51.4 (expected 49.4, previous 50.8); UK March flash manufacturing PMI also came in at 51.4 (expected 50.1, previous 51.7) — both above expectations, bullish for gold, silver, and cryptocurrencies.

2. Industry Update

1) March 10: Token 2049 Dubai organizers announced that due to escalating tensions in the Middle East, the conference scheduled for late April this year has been postponed by one year.

2) March 11: Forbes latest billionaire rankings show that Binance founder Changpeng Zhao (CZ) has a net worth of approximately $110 billion, up $47 billion from last year, ranking 17th globally and surpassing Bill Gates.

3) March 11: Market news: Mastercard has launched a new blockchain payments initiative, with Binance, PayPal, and Ripple joining.

4) March 12: Goldman Sachs has become the largest holder of an XRP spot ETF; analysis suggests “super fans” may make up the core investor base.

5) March 13: China’s National Computer Network Emergency Response Technical Team/Coordination Center issued a security risk alert for OpenClaw.

6) March 14: A whale holding LINK for eight years is suspected to have fully exited its position, with a return rate of up to 2,635%.

7) March 15: PostFinance Switzerland expanded its crypto trading services, adding assets such as ARB, NEAR, and SUI.

8) March 16: Paraguay’s national power company planned to use confiscated mining machines to launch a government-led Bitcoin mining project.

9) March 18: A delegate to China’s National People’s Congress stated that domestically developed blockchain infrastructure has been applied across 16 central government ministries and 27 centrally administered state-owned enterprises.

10) March 19: Hana Financial Group and Standard Chartered signed an MoU to collaborate on expanding digital asset businesses.

11) March 21: 10x Research founder Markus Thielen stated that the current Bitcoin rally is mainly driven by heavy selling of put options with strike prices around $55,000 and $60,000.

12) March 21: It was reported that FTX would redistribute $2.2 billion to creditors on April 30.

13) March 23: Liquidity in South Korea’s crypto market has declined, with investors shifting toward equities.

3. Regulatory Policy Update

- Region: The U.S. Internal Revenue Service (IRS) introduces a new form for cryptocurrency audits [U.S.] → [Regulatory guidance issued, implementation details underway]

- Focus: Canadian regulators revoke the registrations of 23 crypto firms in a single move [Exchange licensing policy]

1) March 10: Thailand intensified anti-money laundering efforts, with local crypto platforms freezing over 10,000 accounts.

2) March 10: Trump threatened to stop signing any legislation until a voter ID bill is passed, potentially affecting the progress of crypto regulatory legislation.

3) March 10: China’s Supreme People’s Procuratorate work report stated that 3,259 individuals were prosecuted in 2025 for money laundering crimes involving virtual currencies and underground banks.

4) March 11: The U.S. CFTC Chair outlined key priorities for the coming years, including clarifying crypto regulations and ending jurisdictional disputes with the SEC.

5) March 11: The U.S. Department of Justice launched an investigation into Iran’s alleged use of Binance to evade sanctions; a federal judge in Alabama dismissed a lawsuit accusing Binance of financing terrorism.

6) March 12: The UK Home Office released its 2026–2029 anti-fraud strategy, identifying cryptocurrencies as a “growing risk”.

7) March 12: The U.S. IRS introduced a new crypto audit form, requiring taxpayers to report their complete cryptocurrency transaction history.

8) March 13: The U.S. imposed sanctions on a North Korean IT worker network involved in crypto money laundering, with nearly $800 million implicated.

9) March 14: A U.S. Senate housing bill includes provisions banning central bank digital currencies (CBDCs).

10) March 14: The Bank of Canada, together with several banks, completed its first tokenized bond pilot.

11) March 16: Japan’s Financial Services Agency planned stricter penalties for unregistered crypto sales, with maximum prison terms proposed to increase to 10 years.

12) March 18: The U.S., UK, and Canada jointly launched “Operation Atlantic” to combat crypto-related fraud.

13) March 19: South Korea’s National Police Agency issued its first guidelines on dark coin management, reducing virtual asset market capitalization by approximately KRW 54.5 billion over the past five years.

14) March 20: Crypto tax evaders in Poland may face punitive tax rates of up to 75%, as the DAC8 directive accelerates tighter regulatory enforcement.

15) March 21: The SEC Chair proposed a crypto regulatory safe harbor framework, including three exemption pathways covering startups and fundraising.

16) March 22: The European Central Bank is recruiting experts to advance the integration of the digital euro with ATMs and card payment terminals.

17) March 22: Canadian regulators revoked the registrations of 23 crypto firms in a single move.

18) March 23: A Kentucky crypto ATM bill introduced new provisions on hardware wallets, criticized as a de facto ban on self-custody.

19) March 24: China issued regulations on integrity in state-owned enterprises, prohibiting the acceptance of assets such as “virtual currencies.”

V. Market Outlook

From March 26 to April 30, the medium-term trading strategy will still be applied: for the BTC spot, maintain the sell order at $135,900, positioning for the view that the current crypto bull cycle is not yet over, followed by a major rebound. Place the buy orders at $52,800, $21,300, and $15,450, respectively.

For the ETH spot, place sell orders at $3,485 and $4,885. Set dip-buying spot orders at $1,240 (keep active) and $815.

Based on the timeline of the previous crypto bull cycle, BTC consolidated sideways for two months and six days at the mid-cycle stage (from May 19 to July 26, 2021). If this pattern repeats in the current cycle, then by April 12 — the day of a potential sharp rally — it would largely indicate that the current crypto bull market has not yet ended and that the uptrend may continue. Of course, the probability of history repeating exactly is low; this merely suggests that such a scenario is possible.

On March 21, CryptoQuant analyst Darkfost noted that altcoin trading volume has continued to decline, reflecting a clear drop in investor interest. Against a backdrop of a bearish market and geopolitical uncertainty, altcoins have persistently underperformed Bitcoin, with risk appetite contracting significantly. Currently, Binance’s daily altcoin trading volume stands at around $7.7 billion, while other major exchanges total approximately $18.8 billion — well below the peaks seen in October 2025 and February (when Binance reached $40–50 billion and other platforms $63–91 billion). Binance currently accounts for about 40% of market share. The analysis suggests that historically, volume peaks often coincide with local market tops and the release of FOMO sentiment, while the current subdued trading environment implies that potential opportunities tend to emerge when market attention is at its lowest.

VI. Risk Alert

1. Macro Risks: [Escalation of geopolitical conflicts]

The U.S. 82nd Airborne Division, along with Marines deployed from Japan to the Middle East, are participating in island-seizure operations, further intensifying tensions in Iran.

2. Industry Risks: [Regulatory crackdowns/surprise inspections]

3. Technical Risks: None at present. [Abnormal whale address activity / Sharp spikes in on-chain gas fees, etc.]

Trading Advice:

Keep spot positions within ≤85% of total capital, and set dynamic take-profit and stop-loss levels to avoid blindly chasing rallies or selling into weakness with high leverage.

Disclaimer: The data in this report are sourced from publicly available information. FameEX makes no representations on the accuracy or suitability of any official statements made by the exchange regarding the data in this area or any related financial advice.